Supplied

Drone attacks on Saudi Arabian oil fields. Heightened tensions in Kashmir. Turkey invading Syrian borderlands. What do these regional conflicts mean for global markets and how should long-term-growth investors approach them? Here we offer a basic primer on how markets have dealt with geopolitical turmoil and the factors we think explain this history.

Markets are no strangers to regional conflict. Sadly, such conflicts are a near-constant during bull and bear markets alike. America’s early 1950s Korean War and the 1962 Cuban Missile Crisis – the 13-day stand-off between the U.S. and the Soviet Union – occurred in bull markets. The 1990s bull market included the first Gulf War as well as the Bosnian War, civil wars in Georgia and Afghanistan and the first Chechen War. The 2003-2007 bull market included ongoing fighting in Iraq and Afghanistan, the conflict between Israel and Hezbollah and other conflicts. The current bull market has endured the Arab Spring, fighting in Eastern Ukraine and the campaign against the Islamic State in Syria and Iraq. Other conflicts, including the Falklands War, the beginning of the war in Afghanistan, the Iran/Iraq War and second Chechen War, began or lasted into bear markets.

Rising tensions and regional conflicts often cause short-term equity-market volatility, but our analysis of past events shows they haven’t caused bear markets. In our view, uncertainty preceding regional conflicts can weigh on equity returns. But once fighting begins, returns often improve. This is not because armed conflict is positive for markets, in our view. Rather, we think it is because the outbreak of conflict ends the uncertainty over whether armed combat will happen. Investors can then assess the situation rationally, see that it affects only a small portion of the global economy, and scale the likely minor impact on corporate profits. Whilst we realize this sounds cold-hearted, markets can seem that way at times, and we think accepting this tendency is key to assessing geopolitical risks correctly.

This tendency is evident in the period surrounding the Korean War’s start, as Exhibit 1 shows.

Exhibit 1: Korean War Tensions Didn’t Cause a Bear Market

Source: FactSet, as of 14/10/2019. S&P 500 Price Index Level in USD, 31/12/1948–31/12/1953. Currency fluctuations between the US dollar and Canadian dollar may result in higher or lower investment returns.Supplied

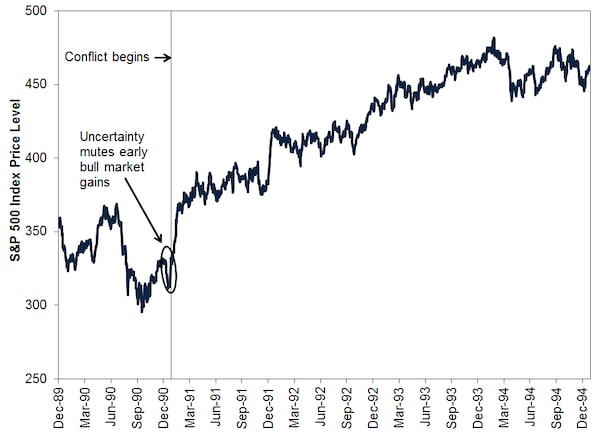

U.S. equity markets were also volatile approaching the start of the Gulf War in January 1991. At the time, global equities were recovering from a bear market, which ran from Jan. 4 until Sept. 28, 1990. [i] Bear markets typically end with a swift rebound, and early on, that recovery was apparently no exception. But beginning in Dec. 1990, as uncertainty over America’s potential intervention into war between Iraq and Kuwait escalated, the recovery paused. Yet even regional conflict including the world’s largest economy didn’t prevent the recovery from resuming after fighting commenced and uncertainty abated.

Exhibit 2: Gulf War Uncertainty Didn’t Derail Markets

Source: S&P 500 Price Index Level in USD, 29/12/1989–29/12/1994. Currency fluctuations between the US dollar and Canadian dollar may result in higher or lower investment returns.Supplied

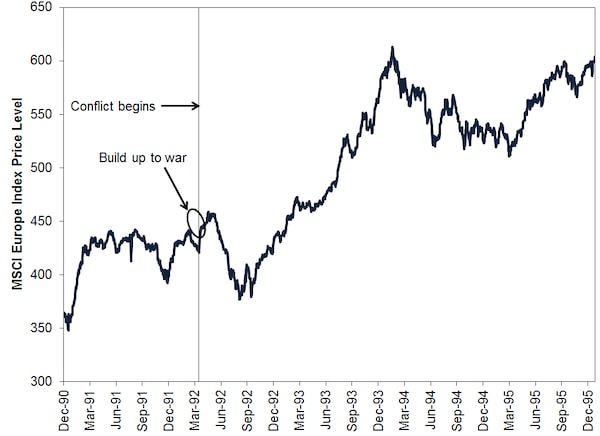

Now, one might argue the Gulf and Korean Wars didn’t derail markets since they weren’t in or near major economic centres. Yet conflicts occurring closer to commercial centres haven’t ended bull markets, either. For example, consider the Bosnian War, which spanned years and occurred on European soil, with terrible destruction and loss of life. The buildup to the War, which officially ran from February 1992 to December 1995, weighed on European markets. Yet they resumed rising shortly after fighting began. The rise was derailed in 1992 by Europe’s currency crisis and the regional recession that ensued. But these economic problems were due to the fallout from countries’ ultimately unsuccessful efforts to defend the European Exchange Rate Mechanism. Equities resumed rising later that year and continued doing so even as the tragic events in former Yugoslavia continued – including the Srebrenica Massacre in 1995.

Exhibit 3: Markets Persevered During the Bosnian War

Source: FactSet, as of 08/10/2019. MSCI Europe Index Price Level in local currencies, 31/12/1990–31/12/1995. Currency fluctuations between local currencies and the Canadian dollar may result in higher or lower investment returns.Supplied

Since reliable equity-market data begin at the end of 1925, only World War II’s onset in Europe was large enough to end a global bull market.

Exhibit 4: World War II and Equity Returns

Source, FactSet, as of 15/10/2019. S&P 500 Index Price Level in USD, 31/12/1937–31/12/1945. Currency fluctuations between the US dollar and Canadian dollar may result in higher or lower investment returns.Supplied

By early 1938, U.S. equities were rebounding from a bear market that had begun in March 1937 tied to monetary policy errors, and the American economy was showing signs of improvement after a recession. Yet the recovery ended right around Germany’s invasion and subsequent annexation of the Sudetenland in Oct. 1938, which made Hitler’s territorial ambitions in Europe clear. We think markets then had to contend with the rapidly rising likelihood of a huge conflict raging across Europe, destroying massive quantities of lives, property and economic output. Even then, the full scope wasn’t clear until France’s shocking fall in May/June 1940. As the War escalated, embroiling most of the Continent, as well as Britain, Japan, Russia and America, equities sank for years. Yet even then, a new bull market began in 1942, three years before the War’s end in 1945.

Whilst data during the World War I era are less reliable, historian Niall Ferguson’s book The Ascent of Money makes a strong case that the Great War had a similar impact.[ii] US equity-market data from that era, though questionable, also show American railroad shares and other companies took a significant hit during the War.[iii] In our view, it takes a huge war, with major powers facing off against each other across a global theatre, for capital markets to suffer heavy-enough losses to cause a bear market.

Therefore, when regional tensions bubble, we think investors are best off asking whether the conflict is likely to go global. Even if a conflict involves major nations, unless the fighting itself spreads across major swaths of the global economy, significantly disrupting trade and output, it likely won’t have the power to sink shares for long.

[i] Source: FactSet, as of 14/10/2019. MSCI World Index price return in USD, 04/01/1990–28/09/1990. Currency fluctuations between the US dollar and Canadian dollar may result in higher or lower investment returns.

[ii] Source: Ferguson, Niall (2008). The Ascent of Money. New York, NY, The Penguin Press.

[iii] Source: FactSet, as of 15/10/2019. Statement based on Dow Jones Industrial Average price returns in 1913 and 1914 in USD. Currency fluctuations between the dollar and CURRENCY may result in higher or lower investment returns.

Fisher Asset Management, LLC does business under this name in Ontario and Newfoundland & Labrador. In all other provinces, Fisher Asset Management, LLC does business as Fisher Investments Canada and as Fisher Investments.

Investing in stock markets involves the risk of loss and there is no guarantee that all or any capital invested will be repaid. Past performance is no guarantee of future returns. International currency fluctuations may result in a higher or lower investment return. This document constitutes the general views of Fisher Investments Canada and should not be regarded as personalized investment or tax advice or as a representation of its performance or that of its clients. No assurances are made that Fisher Investments Canada will continue to hold these views, which may change at any time based on new information, analysis or reconsideration. In addition, no assurances are made regarding the accuracy of any forecast made herein. Not all past forecasts have been, nor future forecasts will be, as accurate as any contained herein

This content was produced by an advertiser. The Globe and Mail was not involved in its creation.