3M(NYSE: MMM) left investors wondering. It's no secret that the industrial sector has been hit by soaring raw material costs, ongoing supply chain issues, and component shortages. Furthermore, end-market weakness in areas like semiconductors and automotive and the effect of the war in Ukraine have all hit the sector. As a result, many industrial companies have lowered full-year guidance ranges or expectations accordingly. However, 3M wasn't one of them. So is that good or bad news? Here's the lowdown.

Image source: Getty Images.

Guidance unchanged

Despite a challenging first quarter and CFO Monish Patolawala noting his caution in the current environment amid disclosing that "We are seeing a slow start to sales in April" during the earnings call, management stuck with its full-year guidance.

As a reminder, 3M's guidance is for organic revenue growth of 2% to 5%, with adjusted earnings per share in the range of $10.75 to $11.25, and for earnings to convert into free cash flow at a rate of 90% to 100%.

Admittedly, the 2% to 5% is a pretty wide range. When pressed about where it expects to be within that range during the conference call, neither Patolawala nor CEO Mike Roman took up the challenge. As a result, investors wonder where 3M's growth will be in 2022.

Growth challenges

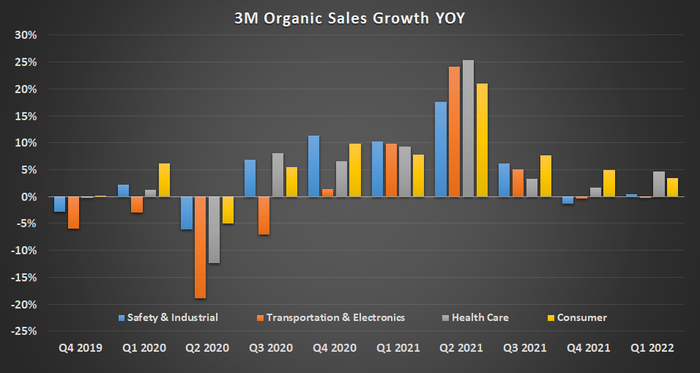

It's a good question because there was no shortage of opposing talking points in the quarter and in 2022 overall. For example, first-quarter year-over-year growth was only 1.7%, and as you can see below, 3M is coming up against some difficult comparisons with the second and third quarters of 2021.

Moreover, as noted above, management said the company had made a slow start to the second quarter. In addition, Patolawala acknowledged that economic growth and industrial production expectations had softened in 2022 due to the uncertain economic and geopolitical environment. That's a significant concern for a company like 3M because its size and spread of end markets mean its revenue growth will always be a function of growth in the industrial sector.

Patolawala said that "Raw materials and logistics costs are expected to be up, impacting Q2 year on year by approximately $225 million" -- something that will squeeze profit margin. On the subject of margin, it's worth noting that management believes "volume gives us the best leverage, so the more we can grow, you're going to get more incremental leverage." In plain English, this means 3M needs sales volumes to generate profit margin expansion significantly. So if volumes fall short of expectations, there could be pressure on its profit margin expansion expectations and profit.

Data source: 3M presentations.

Stock-specific issues

There are also question marks around the company's specific end market exposures. The chart above shows the segmental organic growth trends, and the table below shows the assumption laid out in the investor meeting in February.

The consumer segment looks to be in line with expectations, but given that 46% of its sales go to the home improvement market, any slowdown in the housing market from rising rates will hurt. The healthcare segment also appears to be on track, but the omicron variant hit elective procedures in the first quarter, and there could be some issues around getting healthcare workers back to work in 2022.

The safety and industrial segment is interesting because the 0.5% growth in the first quarter would have been 2% if not for a 1.5% year-over-year decline in disposable respirator sales. That's a better result (for respirators) than management had expected going into the quarter. Then again, it might have come down to the effect of the omicron variant in January and February.

However, the biggest concern is around the transportation and electronics segment. Patolawala noted that "growth expectations for Transportation and Electronics end markets have moderated" primarily due to a reduction in global light vehicle production expectations in 2022. In addition, recent weakness in semiconductors and smartphone production is threatening growth prospects for the segment.

Indeed, management gave such a wide guidance range for the segment's growth in 2022 because of uncertainty in the segment's end markets. Therefore, given the turn for the worse, it's reasonable to expect growth at the lower end of the range for 2022.

3M | Q1 Actual | Full-Year Growth Outlook |

|---|---|---|

Safety & Industrial | 0.5% | Flat to low single digits |

Transportation & Electronics | (0.3)% | Low to high-single digits |

Health Care | 4.7% | Mid-single digits |

Consumer | 3.4% | Low to mid-single digits |

Total | 1.7% | 2%-5% |

Data source: Company presentations.

What it all means for investors

3M's revenue and earnings guidance is under pressure, and anyone buying the stock for its 4.1% dividend yield should bear that in mind before buying in. That's not to say the stock is unattractive for investors seeking a long-term entry point into a great company; just be aware that there could be some negative near-term news to come in 2022.

10 stocks we like better than 3M

When our award-winning analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and 3M wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of April 7, 2022

Lee Samaha has no position in any of the stocks mentioned. The Motley Fool recommends 3M. The Motley Fool has a disclosure policy.