If you follow the Canada Food Guide, then you are faced with a new personal finance challenge.

The recently updated version of the guide emphasizes eating vegetables and fruit (there’s a picture of a plate half-covered by fruits and vegetables, with one-quarter devoted to protein and another to whole grain foods). But fresh produce can be expensive for a couple of reasons. One, prices can spike higher seasonally or if harvests are affected by bad weather (remember the $7 cauliflower?). Two, some veggies and fruit have a short shelf life and may rot before you get your money’s worth.

Page from Canada's Food Guide. Credit: Health CanadaHealth Canada

A blog called The Financial Diet has the answer: Frozen fruits and vegetables. Buying frozen eliminates the problem of letting produce go to waste, which means you get more value. Worried that you’re losing nutritional value when you buy frozen produce? Research shows that you don’t. In fact, peas and green beans offered more nutrients in frozen form, possibly because they were packaged when ideally fresh.

Aside from frozen vegetables and fruit, the Financial Diet blogger keeps week-to-week grocery costs under control by eating 100 per cent vegetarian at home, by keeping the same favourite meals in heavy rotation and by doing the advance planning necessary to get dinner ready quickly on busy nights. That’s how you avoid the Skip the Dishes solution.

Subscribe to Carrick on Money

Are you reading this newsletter on the web or did someone forward the e-mail version to you? If so, you can sign up for Carrick on Money here.

Rob’s personal finance reading list…

“No nursing home for us”

A Facebook post by a guy named Terry Robison went viral recently. Mr. Robison joked that he and his spouse will be checking into a Holiday Inn rather than a nursing home. He’s done the math and it’s cheaper to live in a hotel than a nursing home. U.S. numbers are used here, but the point is valid. Long-term care is expensive. Hey, I wrote a column on that just recently.

F.I.R.E. fizzled for him

A Londoner reports on his experience living the frugal life of the F.I.R.E. adherent – financial independence, retire early. Let’s just say he tried it and didn’t like it.

Most – and least – reliable cars

If you’re in the market for new car or truck, you’ll want to consult these Consumer Reports Top 10 lists of vehicles that offer the best and worst reliability.

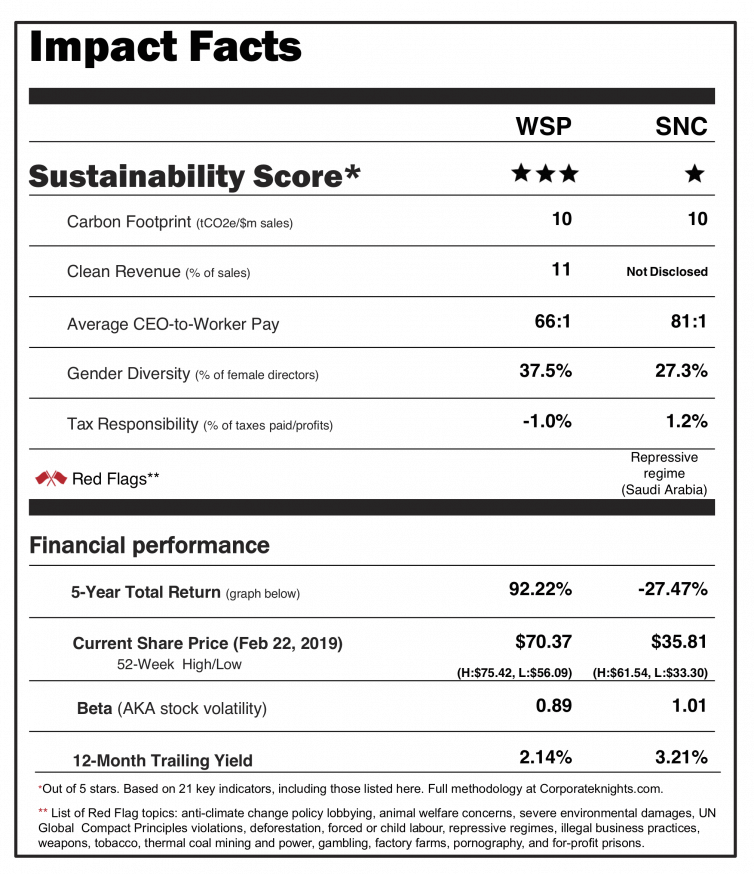

An investor’s take on SNC-Lavalin

Say what you want about SNC, but it does offer a rare investment opportunity for Canadians as a result of its global reach as an engineering and construction company. Want an alternative company to consider? Corporate Knights, the self-described “magazine for clean capitalism,” has created a head-to-head comparison of SNC and WSP Global Inc., also a global engineering firm based in Canada.

Today’s financial tool

An online tool to help you answer the question, “pay down debt or invest?”

Ask Rob

Q: Rob, I am a senior and I have a small amount of principal in RRSP. My beneficiaries are my children. When I die, the whole amount in the RRSP will be subject to tax in my final tax return. That's not a problem as I have a life insurance policy to cover the tax bill. My concern is the state of the markets upon my death. If the equities markets are down all my careful investing acumen may be diminished; a situation beyond my control. My question is, can the holdings be transferred in kind to my children, so long as they pay the taxes due?

A: I enlisted some help on this one from John Natale, head of tax, retirement and estate planning services at Manulife. His reply: “The holdings can be transferred in kind to your children but will be included in your income as a taxable withdrawal from your RRSP and you will have to pay the tax. Your children will receive the holdings tax-free and the fair market value of the holdings at the time of the transfer will serve as the children’s adjusted cost base going forward. While the tax liability rests with you, if your children agree, they could gift you funds to cover the payment.”

Do you have a question for me? Send it my way. Sorry I can’t answer every one personally. Questions and answers are edited for length and clarity.

What I’ve been writing about

- Parents financially supporting thirtysomething kids? It’s happening

- “I’m hesitant to invest right now because stocks are expensive” (for Globe Unlimited subscribers)

- Rob Carrick’s 2019 ETF Buyer’s Guide: Best U.S. equity funds (for Globe Unlimited subscribers)

More Carrick and money coverage

For more money stories, follow me on Instagram and Twitter, and join the discussion on my Facebook page. Millennial readers, join our Gen Y Money Facebook group. Send us an e-mail to let us know what you think of my newsletter. Want to subscribe? Click here to sign up.

Rob Carrick

Rob Carrick{kind=link}