In 2015, the BC Securities Commission wanted to fine Peter Harris more than $2.1-million and ban him from the capital markets for life after investors lost millions on a fraudulent health-foods stock he touted.

But Mr. Harris just laughed it off.

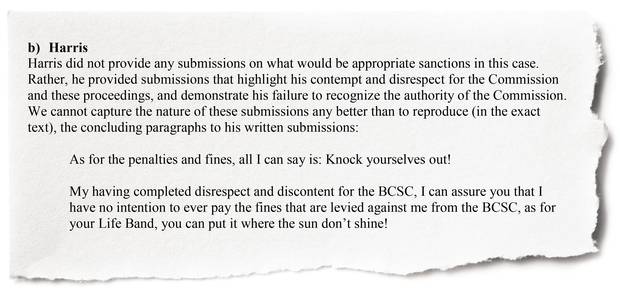

In a written response to the BCSC, he told the regulator it could do whatever it wanted – he couldn't care less.

"As for the penalties and fines, all I can say is: Knock yourselves out! My having complete disrespect and discontent for the BCSC, I can assure you that I have no intention to ever pay the fines that are levied against me," Mr. Harris said.

"As for your life ban, you can put it where the sun don't shine!"

And there was little the BCSC could do in response.

Mr. Harris knew the administrative penalties imposed by Canada's securities regulators were difficult to enforce and that he could likely walk away without paying a single penny – and so he did. But he's far from alone.

An investigation by The Globe and Mail has determined that the amount of unpaid securities fines in Canada is more than $1.1-billion, a massive figure that shows just how many of these sanctions are being ignored among white-collar criminals and fraudsters, and how toothless the regulators are in their ability to collect.

Canada's financial regulators don't keep national figures on delinquent fines, so The Globe decided to calculate them independently: A year-long data analysis of nearly 6,000 case files across all of Canada's securities regulators, some of which have records stretching back 30 years, was cross-referenced with the delinquent-fines databases kept by each regulator. The analysis shows the amount of fines being flouted in Canada has reached $1,101,583,984.44.

However, The Globe was unable to obtain complete historical data on unpaid fines from every regulator, so the true number is likely even higher.

A billion dollars would be more than enough to pump badly needed funds into the budgets for white-collar criminal investigations across Canada, or even return some losses to investors who the regulators are mandated to protect – if only that money was being collected.

The number is also increasing, having risen 22.5 per cent from just two years ago, according to The Globe's national calculation, as regulators collectively mete out more than $100-million in new fines each year, often using them to generate bold headlines on news releases designed to make the system appear tough on crime.

That total figure includes all unpaid fines issued against individuals, as well as shared fines levied against groups of offenders and sanctions aimed at companies.

In order to get a clearer sense of the problem, The Globe built an algorithm to analyze the databases kept by each securities commission across the country to determine how many unpaid fines are solely levied against individuals.

The analysis found that there are 1,009 individuals who collectively owe more than $619-million securities commissions are unable to collect.

The average unpaid fine for these individuals is $613,965.60.

Meanwhile, collection rates at the regulators are abysmal, sometimes as low as single digits in some jurisdictions.

The unpaid-fines number is just one of several troubling issues uncovered in The Globe's investigation into the oversight of Canada's capital markets. The thousands of case files analyzed also reveal that one in every nine people sanctioned in Canada usually ends up with another blemish on their record, suggesting that committing such crimes is easy and that little exists in the way of effective deterrence for repeat offenders.

At the same time, these people appear to be exploiting Canada's patchwork of provincial regulators. More than 63 per cent of repeat offenders have been previously sanctioned in another jurisdiction, or by a different regulator, the analysis shows.

For the victims of financial crime, those figures are upsetting. Debra McFadden, an Ontario woman whose elderly relatives were ripped off by a fraudulent adviser who escaped without paying fines, calls the number of delinquent fines "a national disgrace."

Ms. McFadden says she gets particularly frustrated when she sees statements such as the one the Canadian Securities Administrators, an umbrella organization for the regulators, issued two years ago on Twitter, claiming: "Fact: $138,293,796 were ordered in fines and penalties in 2015," while failing to mention that only a fraction of that money is ever collected.

"To me, that is a lie by omission, and you're fostering a misconception for the public that these fines are actually doing something and that people can feel reassured that, 'Boy, the regulators are on the job here,'" Ms. McFadden said.

"The fines are not a deterrent."

"Always one step behind"

Canada's securities regulators say it is difficult – and sometimes impossible – to collect on the fines they issue. The perpetrators of stock-market crimes often have no assets, have spent all the money or have hidden the funds where they can't be reached – either offshore or cloaked behind another person's name.

"It's a complicated process," Douglas Muir, director of enforcement at the BCSC, said of the difficulty of collections. "There may be a conception that these people bring in the money and they leave it sitting around, a large pot of money, and all we have to do is go pick it up if we could just be bothered to go and do that.

"It's not that at all. The money's often long gone before we even hear about the misconduct."

But some, such as Ms. McFadden, wonder how hard the regulators are working to find that money.

In its most recent annual report, the BCSC said it had $478-million worth of unpaid fines against individuals, companies and groups as of March 31, adding that it expects only $100,000 of that – or 0.02 per cent – is likely collectible.

While B.C. typically doles out the largest sanctions, which inflates its numbers, the delinquency picture is not remarkably better among the other major securities commissions. The OSC has the second-highest amount of unpaid fines, with $360-million, followed by the Alberta Securities Commission, which is third at nearly $109-million. (A complete set of numbers was not available from Quebec's main capital markets regulator, but their unpaid amount for the past three years sits just shy of $40-million.) "I realize the collection rates generally in securities matters are quite dismal, I acknowledge that," said Cynthia Campbell, director of enforcement at the Alberta Securities Commission.

While the U.S. Securities and Exchange Commission reports higher collection rates than all regulators in Canada – sometimes upward of 40 per cent in certain years – Ms. Campbell notes the U.S. regulator will write off fines it figures it can't collect, a practice that takes large numbers off the books. That isn't done in Canada.

"The majority of situations, when we bring a case forward, the damage is done … the money has been spent, or has been funnelled into a jurisdiction where we can't access it," Ms. Campbell said. "So, you're trying to get blood from a stone."

However, because Canada's fines are most often issued through a regulatory tribunal, where the cases are easier to win than in criminal court, there is no jail time attached to the ruling and very little recourse for regulators to collect. That means there is often nothing to prevent the offenders from simply walking away unpunished.

Declaring bankruptcy is often more than enough to stymie regulators.

"We have one case, it was an insider-trading case, where the defence was, 'I have so much money, I would never need to trade on an insider basis.'" James Sinclair, general counsel for the OSC, said. "We were successful, then he filed for bankruptcy – where did the money go?"

But the regulators' assertions that these fines go unpaid because there are no assets or money for the provinces to seize is questionable. In some cases, there appear to be assets hiding in plain sight.

The Globe examined two-dozen sample cases across the country involving known offenders with delinquent fines and found at least four instances in which assets can be traced to the person, such as houses, condominiums, or investment properties, either directly or through joint ownership.

One of those cases involves Lino Novielli, a Toronto man who was caught breaking securities laws in five provinces, but has yet to pay any of his fines.

In 2008, Saskatchewan's financial regulator caught Mr. Novielli and three other men selling unregistered stock in a junior mining company, GoldPoint Resources Corp. Rather than penalize him immediately, Mr. Novielli got off easy. He was ordered to stop the illegal sales – and signed a written undertaking with the regulator that he would not continue. But the ink barely had time to dry on that agreement before Mr. Novielli and his cohort began to distribute the fraudulent shares in the province again, according to regulatory documents.

When the OSC later caught the group using false claims and high-pressure sales tactics in Ontario, raking in nearly $1.7-million, the regulator hit Mr. Novielli and others at the company with almost $3-million in fines, including a $300,000 fine issued directly to him. None of those sanctions have been paid.

Despite the OSC's claims that it works hard to collect on sanctions and to recoup funds for investors, The Globe found Mr. Novielli and his wife (who also owes the OSC $300,000 in unpaid penalties) own a large house in an upscale bedroom community north of Toronto. At the beginning of 2016, the house had an assessed value of $1,124,000, according to municipal records.

When The Globe visited the house recently to discuss the fines with Mr. Novielli, a voice on the intercom said, "I don't think he wants to comment."

The woman, who later identified herself by phone only as Mrs. Novielli, said Mr. Novielli was "not in the country." Asked about the fine, which is still delinquent, she said, "as far as we're concerned, restitution's been paid."

She did not elaborate, but referred further questions to a lawyer, who could not be reached. According to OSC files, Mr. Novielli was sentenced in October to 10 months in jail for breaching a cease trade order against him.

The Globe’s analysis shows toothless penalties for misconduct fail to act as an effective deterrent for offenders. Without this deterrent, consumer faith in the market can suffer, says Anita Anand, a law professor at the University of Toronto who specializes in securities legislation. Prof. Anand is seen at the University’s Jackman Law Building on Dec. 11.

Mark Blinch/The Globe and Mail

When it comes to unpaid fines, the OSC said the enforcement problem is partly attributable to how much time and effort it takes to conduct asset searches.

"The average investigation is probably 750 hours. We've had collection cases where we've been probably double that. And the time we spend chasing some assets around the globe is time we're not spending chasing the next bad guy," Mr. Sinclair said. "So that's also a challenge."

The OSC recently hired an outside law firm to act as a collections agent, he said.

"We're trying to make life uncomfortable, but we're never going to be perfect. … We're always one step behind."

This lack of enforcement is harmful to the public's confidence in the markets, said Anita Anand, a law professor at the University of Toronto, who specializes in securities legislation.

"That's a problem if deterrence is one of the ways in which you ensure that markets function with integrity," Prof. Anand said. "That's a problem if you believe investors need to have confidence in the capital markets before they place their money in those markets."

"Why would you pay?"

Across Canada, a majority of unpaid fines can be traced to a relatively small number of people who refuse to pay.

The Globe's analysis of delinquent fines at regulators around the country indicates the largest penalties handed out to the worst offenders – the sanctions intended to send the strongest message of deterrence – are also often the least likely to be paid.

But if this small number of cases were resolved, it would have a dramatic effect.

Of the 1,009 individuals that owe a combined $619-million in fines in Canada, just 23 people are responsible for slightly more than half of that amount (50.8 per cent) across the country.

In British Columbia, seven people account for 50.2 per cent of the $340-million worth of fines levied against individuals, while in Ontario, nine people account for 50.9 per cent of the $139-million owed by individuals.

The distribution of unpaid fines

A majority of unpaid fines across most

jurisdictions are concentrated in just a small

number of people. The BCSC has the most

lopsided distribution of unpaid fines, with more

than 50% of fines attributable to just 7 people.

Number of people owing…

50% of fines

70% of fines

90% of fines

British Columbia Securities Commission

248

7

15

30

People with unpaid fines

Account for 90% of unpaid fines

Account for 70% of unpaid fines

Account for 50% of unpaid fines

Mutual Fund Dealers Association

234

10

30

88

Ontario Securities Commission

209

9

25

75

Investment Industry Regulatory

Organization of Canada

188

14

38

97

Alberta Securities Commission

107

9

17

44

Note: Unpaid fine distributions were calculated using

only individual, personal fines. All joint fines were ignored.

THE GLOBE AND MAIL, SOURCE: REGULATORS

The distribution of unpaid fines

A majority of unpaid fines across most jurisdictions

are concentrated in just a small number of people. The

BCSC has the most lopsided distribution of unpaid fines,

with more than 50% of fines attributable to just 7 people.

Number of people owing…

50% of fines

70% of fines

90% of fines

British Columbia Securities Commission

248

7

15

30

Account for 90% of unpaid fines

Total number

of people with

unpaid fines

Account for 70% of unpaid fines

Account for 50% of unpaid fines

Mutual Fund Dealers Association

234

10

30

88

Ontario Securities Commission

209

9

25

75

Investment Industry Regulatory Organization of Canada

188

14

38

97

Alberta Securities Commission

107

9

17

44

Note: Unpaid fine distributions were calculated using only individual,

personal fines. All joint fines were ignored.

THE GLOBE AND MAIL, SOURCE: REGULATORS

The distribution of unpaid fines

A majority of unpaid fines across most jurisdictions are concentrated in just a small

number of people. The BCSC has the most lopsided distribution of unpaid fines, with

more than 50% of fines attributable to just 7 people.

Number of people owing…

50% of fines

70% of fines

90% of fines

British Columbia Securities Commission

248

7

15

30

People combined account for 90% of unpaid fines

Total number

of people with

unpaid fines

People combined account for 70% of unpaid fines

People combined account for 50% of unpaid fines

Mutual Fund Dealers Association

234

10

30

88

Ontario Securities Commission

209

9

25

75

Investment Industry Regulatory Organization of Canada

188

14

38

97

Alberta Securities Commission

107

9

17

44

Note: Unpaid fine distributions were calculated using only individual, personal fines.

All joint fines were ignored.

THE GLOBE AND MAIL, SOURCE: REGULATORS

The distribution of unpaid fines

A majority of unpaid fines across most jurisdictions are concentrated in just a small number of people.

The BCSC has the most lopsided distribution of unpaid fines, with more than 50% of fines attributable to just 7 people.

Number of people owing…

50% of fines

70% of fines

90% of fines

British Columbia Securities Commission

248

7

15

30

People combined account for 90% of unpaid fines

Total number

of people with

unpaid fines

People combined account for 70% of unpaid fines

People combined account for 50% of unpaid fines

Mutual Fund Dealers Association

234

10

30

88

Ontario Securities Commission

209

9

25

75

Investment Industry Regulatory Organization of Canada

188

14

38

97

Alberta Securities Commission

107

9

17

44

Note: Unpaid fine distributions were calculated using only individual, personal fines. All joint fines were ignored.

THE GLOBE AND MAIL, SOURCE: REGULATORS

The distribution of unpaid fines

A majority of unpaid fines across most jurisdictions are concentrated in just a small number of people.

The BCSC has the most lopsided distribution of unpaid fines, with more than 50% of fines attributable to just 7 people.

Number of people owing…

50% of fines

70% of fines

90% of fines

British Columbia Securities Commission

248

7

15

30

People combined account for 90% of unpaid fines

Total number

of people with

unpaid fines

People combined account for 70% of unpaid fines

People combined account for 50% of unpaid fines

Mutual Fund Dealers Association

234

10

30

88

Ontario Securities Commission

209

9

25

75

Investment Industry Regulatory Organization of Canada

188

14

38

97

Alberta Securities Commission

107

9

17

44

Note: Unpaid fine distributions were calculated using only individual, personal fines. All joint fines were ignored.

THE GLOBE AND MAIL, SOURCE: REGULATORS

Vincent Ciccone of Cambridge, Ont., is among them. His company, Ciccone Group Inc., once billed itself as "one of the fastest growing niche financial venture companies in Canada."

The company, purportedly an investment fund, lured investors by promising fat returns of more than 20 per cent. As word got out in the Waterloo region, dozens of people gave him their retirement savings to invest. But in reality, the so-called fund was nothing more than a Ponzi scheme. Investors were paid small dividends early on, to give the appearance that profit was being made, but in fact, Mr. Ciccone and others were using much of the money for their personal use. Cash flowing in from new investors helped keep the ruse going.

"Other than using the proceeds to pay interest and redemptions to investors, proceeds from the distributions were directed to business ventures that Mr. Ciccone was involved in, to charities, or loaned to friends," the OSC said in regulatory files.

There was no prospect "of ever generating the returns of over 20 per cent stated in the promissory notes that Ciccone and the Ciccone Group sold to investors."

When the facade was shattered, 160 investors had lost more than $120-million.

In 2012, the OSC levied $850,000 in fines againts Mr. Ciccone and ordered him to surrender $15.5-million to investors. Mr. Ciccone was later convicted of fraud and sentenced to five years in prison on criminal charges. But none of the fines issued by the securities regulator – more than $16.3-million in penalties – have been paid.

However, a search of property records by The Globe turned up documents that show Mr. Ciccone's wife sold a house in Cambridge in 2013 for $437,500. It is not clear where that money went.

It's a tiny sum compared with the millions of dollars Mr. Ciccone's victims have lost. But, somehow, the proceeds from that house sale don't appear to have made their way back to the bilked investors. Not a cent of his massive sanction, including the order to compensate those who lost money, has been paid.

Meanwhile, Mr. Ciccone declared bankruptcy and a trustee has been placed in charge of his assets.

In interviews, several securities regulators said that even if the fines aren't collected, issuing them sends a message of deterrence to others who might consider committing securities crimes.

In the past decade, seven securities regulators – including those in B.C., Alberta, Saskatchewan, Manitoba, Ontario, New Brunswick and Nova Scotia, as well as the Investment Industry Regulatory Organization of Canada (IIROC), which represents investment dealers, and the Mutual Fund Dealers Association (MFDA) – have posted lists on their websites detailing offenders who haven't paid their fines.

The strategy has garnered some success, said Ms. Campbell in Alberta, where the list is two years old. "We've had two cases since we've brought it in, where individuals immediately after an administrative proceeding came to us and said, 'I want to pay my penalty now so I don't get on that list,'" Ms. Campbell said. "That was their motivation for making the payment, the administrative penalty. That hadn't happened previously."

Still, the introduction of the list has only seen a handful of names removed, while more than 100 remain.

Those who study white-collar crime in Canada are doubtful the strategy is working. The so-called "name-and-shame" lists, as they have been dubbed on Bay Street and elsewhere, have done little to stop the overall trend.

"The next offender is also aware there's no recourse … They [the regulators] have got to figure out a way to make it hurt," Sofia Johan, an instructor at York University's Schulich School of Business, said.

"Would you pay? Why would you pay if there's no other punishment? … I wouldn't pay."

The trauma of a hearing

Some regulators appear resigned to the fact fines won't be paid.

Among the case files analyzed, The Globe found a reference in MFDA documents in which the fact a sanction couldn't be enforced was discussed openly at the hearing.

In that case, an offender asked the panel adjudicating the hearing not to issue a fine because they were already being banned from the industry. And because they were being exiled from the mutual-fund business, there would be no incentive to also pay a fine.

"It is true," the panel said, apparently acknowledging the request's logic. "The imposition of a permanent prohibition may well make it less likely that a fine will ever be paid."

But the MFDA panel issued the fine anyway, along with the ban, because it argued both were warranted.

Investor advocates such as Ms. McFadden see such statements from the regulator as a clear signal to offenders that the fines are unenforceable and represent an acknowledgment that the system doesn't work.

"Why state that in a written public document?" Ms. McFadden said.

There are also cases where those accused of financial misconduct appear to be given sympathetic treatment, which upsets victims such as Ms. McFadden.

In a 2014 IIROC case involving an adviser who caused her clients to lose significant amounts of money, the panel adjudicating the hearing appeared to go easy on the accused.

The adviser, Lucy Lukic, recommended her clients purchase securities in an "off-the-book" investment fund, which was in fact far riskier than investors were told.

Not only was the transaction hidden from her employer and completed without necessary paperwork, such as a prospectus, the investment was actually a fund owned and promoted Ms. Lukic's husband, according to IIROC documents.

The group who bought into the fund, which also included Ms. Lukic and her husband, lost $3-million.

Despite her conflict of interest and questionable conduct, she was ordered to pay $95,000 in fines and was spared a suspension by IIROC. In making its decision, the panel overseeing the hearing took into account that Ms. Lukic had suffered "trauma" by being subjected to a hearing.

That unusual decision by the three-person panel, which was made up of one member from the legal profession and two industry representatives, prompted IIROC's lawyers to appeal to the OSC, which oversees the regulator.

In 2015, the decision was overruled: Trauma experienced by the accused from participating in a regulatory hearing was not a mitigating factor, the OSC said.

Instead, Ms. Lukic was handed a two-year ban from the industry. She could not be reached for comment, but according to IIROC's list of delinquent fines, her penalty has been paid.

"We appealed that to the OSC … because we disagreed with that principle – that trauma was a relevant principle on sanctions," Charles Corlett, IIROC's director of enforcement litigation, said.

"I need help"

Pastor Paul Edwards is still waiting for his money to be returned. As a man of faith, he has long preached about forgiveness. But it became more difficult a few years ago after hundreds of members of Toronto's Caribbean community lost a significant portion of their savings to a fraudulent investment scheme.

In 2007, Mr. Edwards and others were persuaded by a member of the congregation at his church to put money into a firm called Prosporex, an investment club that promised attractive returns of up to 20 per cent a month.

Though many of the people targeted were not well off financially, Prosporex was happy to line up lending for anyone who wanted to invest.

Word of the attractive investment opportunity soon spread, with up to 800 people ultimately investing in what they believed was a legitimate, provincially regulated financial company. Mr. Edwards invested $15,000. Other members of the community scraped together what they could. All told, 1,700 people invested $29-million in Prosporex.

Those who invested were told their funds were being placed in foreign-exchange contracts and were given regular updates showing their account balance increasing. But the statements were fake. The OSC found as much as $20-million of the funds were used for purposes that had nothing to do with investing.

While about $5.3-million of the principal was paid out to investors as false returns, as a way to make the scam appear legitimate, beyond that, "there were no such returns; no profits were ever obtained," the OSC said.

The regulator later found that $14.7-million of the money went into the personal accounts of the men running the scheme, or was moved offshore. Much of it simply went missing.

Sedwick Hill, one of the men behind Prosporex, was accused of pocketing some of the money for himself and, in 2011, the OSC fined the self-purported financial adviser $4.2-million for his role in "a scheme that wrought financial havoc" on its victims. Two other men who worked with Mr. Hill were fined $4-million.

Sedwick Hill, seen in Scarborough, Ont., in November, 2012, was one of the men behind Prosporex, an investment club that promised attractive returns of up to 20 per cent. In an investigation, the OSC found that of the roughly $29-million invested in the venture during 2007, $20-million had been used for purposes other than investing. Mr. Hill was accused of pocketing some of the money for himself and, in 2011, the OSC fined the self-purported financial adviser $4.2-million for his role in ‘a scheme that wrought financial havoc’ on its victims. Mr. Hill’s fine remains unpaid today, and registers among the largest on file with the OSC.

Galit Rodan/The Globe and Mail

"Most of the individual investors lost their investment with calamitous results for themselves and their families," the OSC said.

As with so many other cases, though, the OSC has been unable to collect.

Mr. Hill's penalty now registers among the top unpaid fines in Ontario, along with that of Mr. Ciccone.

According to a land title search, Mr. Hill co-owns a house in Pickering, Ont., but records show the property is heavily leveraged. The house was assessed at $607,000 last year, but the $270,000 mortgage, along with a few liens placed against it – including one for $413,000 by the Minister of National Revenue in 2011 – means there is nothing for the OSC to go after.

As creditors go, the OSC ranks behind the federal government and banks in terms of the agency's power to claim assets.

"The OSC is what is referred to as an 'unsecured judgment creditor,' which means we rank below the CRA and secured lenders, such as banks providing mortgages," a spokeswoman for the regulator said. "Once those creditors are paid, anything remaining is distributed to unsecured judgment creditors."

There's usually not much left.

Sometimes, the regulator can seek to push the person into bankruptcy in order to extract payment through liquidation. But it doesn't always work. "Some of the files aren't big enough to get the [bankruptcy] trustees that interested," the OSC's Mr. Sinclair said. "That's part of our problem."

Even though the securities commission alleges Mr. Hill and others made millions from the scheme, it has no idea where that money went. Mr. Hill could not be reached for comment.

Almost a decade later, Mr. Edwards is still bitter about the situation, with no hope that the steep fines imposed by the OSC will help alleviate the damage caused to him and others.

"Nothing," Mr. Edwards said, when asked what became of the OSC case.

Asked how much money has been recovered, his answer is the same. "Nothing."

Although details of victims are often scrubbed from regulatory documents in accordance with privacy laws, they are numerous.

The Globe reviewed several dozen victim statements filed with the Small Investor Protection Association (SIPA), a Toronto-based organization, to document the toll such crimes take on the public.

One file in particular, a voice-mail left by an elderly woman who lost her retirement savings to an unscrupulous financial adviser, is particularly jarring.

The voice on the line is frail and quivering. The woman is crying and at times she can barely be understood through her tears.

"I'm not doing well," she said. "I just can't accept it. And it's on my mind all the time, and there's nobody to help … I need help."

In this voicemail message left for the Small Investor Protection Association, a victim of securities fraud opens up about her struggles after being defrauded. This message has been edited slightly for brevity and for privacy reasons.

The upper hand

After watching her elderly family members robbed of money in a case in which the fines issued were never paid, Ms. McFadden wonders what the point is of issuing fines that aren't enforced.

"If you don't follow through, you lose your power," she said. "This is exactly where our regulators are."

Jeff Kehoe, director of enforcement at the OSC, said finding a way to collect more fines is "the holy grail" for the regulator. "We will try to do it differently, and we will try to improve," he told The Globe in an interview.

But until the provincial securities commissions get tougher in pursuing more cases through the courts each year, little will happen, according to Richard Powers, a business professor at the University of Toronto who specializes in corporate law and ethics.

"Until jail becomes part of the sanction, where's the incentive to pay?" Prof. Powers said. "The sanctions right now don't pose the same kind of deterrent."

In interviews with several of Canada's biggest financial regulators, The Globe asked what specific tools they needed from the provinces, or from the federal government, in order to better enforce their penalties. None could give a definitive answer.

Poonam Puri, a law professor at York University who specializes in securities regulation, wonders whether enough resources are being devoted to enforcing regulatory orders. "Perhaps more effort needs to be put into that," she said.

Prof. Puri suggests one fix could be to make each settlement with an offender contingent on the payment of fines at the time the agreement is struck.

"The unpaid-fine problem can be addressed in a couple of different ways," Prof. Puri said.

"One way might be to consider having whatever the agreed-to fine is on the table and delivered at the time that the settlement agreement is approved."

Until such changes are made and the regulators pursue their actions more aggressively, they are left with the offenders having the upper hand.

Scofflaws such as Peter Harris, who told the BCSC in 2015 to stick its proposed ban "where the sun don't shine!" stand out for their theatrics. But situations in which the person being sanctioned shows no fear of punishment are surprisingly easy to find.

When the BCSC tried to send a strong message to Leonard William Friesen, a salesman at Canadian Global investment Corp., for selling unsuitable, high-risk securities to several of his clients, the regulator's plan also backfired.

Mr. Friesen was handed a two-year ban from trading securities and prohibited from being a salesperson until he met "certain proficiency requirements." He was also fined $20,000.

But Mr. Friesen disagreed with his penalty – believing it was too harsh. So he refused to pay that amount and, instead, asked the BCSC to reconsider.

One year later, the regulator caved and lowered his fine to $5,000, hoping he would pay that amount. He didn't.

Five years after that, Mr. Friesen came back and asked for the fine to be forgotten altogether. This time, the BCSC stood its ground. And then nothing happened.

Fifteen years after he was sanctioned, Mr. Friesen's fine – much like the $1.1-billion worth of penalties being flouted across Canada – remains unpaid.

With research by Rick Cash

Read the background on our data-reporting process at tgam.ca/money-methodology

Are you a victim of securities fraud, or have a tip you'd like to pass on? Share your story: grobertson@globeandmail.com and tcardoso@globeandmail.com

This is the third and final part of an investigative series on white-collar crime and abuse in the Canadian capital markets.

EASY MONEY: MORE IN THE SERIES