Briefing highlights

- Toronto condo market ultra tight

- Economic growth slows to 1.7%

- Unemployment dips below 6%

- Canadian dollar spikes on report

- National Bank raises dividend

- Markets at a glance

- What Merkel’s woes could mean

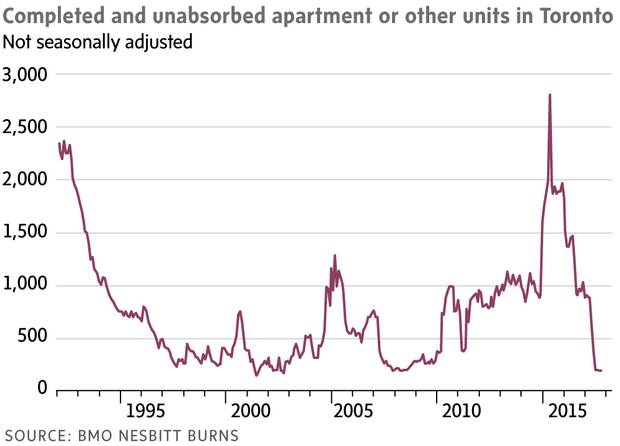

Cupboard bare

Toronto's new condo market has become exceptionally tight, buoying prices while the rest of the real estate market slumps.

Add that to the list of worries already plaguing the area's housing market.

Canada Mortgage and Housing Corp. numbers show just 197 new condo units in the "standing inventory" in the Toronto area in October, noted Bank of Montreal senior economist Sal Guatieri.

Among those, a look at the CMHC numbers show, 186 are in the immediate area, with just 11 in neighbouring communities such as Oakville, Markham and Richmond Hill.

Those 197 represent "about a quarter of the long-run mean and fewer than in drum-tight Vancouver," Mr. Guatieri said.

"By comparison, there are more than 1,000 unsold units available in Montreal and Calgary. The market has come a long way from the apparent glut in 2015."

While the rest of the housing market is suffering, though bottoming, in the wake of new provincial measures to tame the overheated region, condo prices are faring just fine.

"The lean supply has helped benchmark condo prices in the resale market sidestep the recent correction in the detached segment, and explains why they are up a honking 23 per cent year over year in October," Mr. Guatieri said in a research note.

"With the condo rental vacancy rate at 0.7 per cent in October (second-lowest on record), rents are also surging as builders can't keep up with demand."

A pedestrian walks past a sign for West Block 1928 Condos in Toronto on May 27, 2017.

Brent Lewin/Bloomberg

The latest numbers from Urbanation, which tracks the city's condo market, showed sales in the third quarter tumbled 30 per cent from a year earlier, but that's because "fewer new projects came to market following an explosive first half that saw new launches more than double and sales soar by 67 per cent," the group said in its late October report.

As for rental units, Urbanation said the slip in vacancy rates as measured by CMHC was expected. But …

"Urbanation has been tracking the dramatic tightening in rental conditions throughout the year, to the point that it came as a surprise that purpose-built vacancy rates weren't less than 1 per cent (a 16-year low) and condo vacancy rates weren't below the reported 0.7 per cent (second-lowest ever recorded," it said earlier this week.

Purpose-built units are those that were planned and constructed with the aim of units being rented.

"Still the 22-per-cent fall in the total number of vacant purpose-built and condo rentals was the steepest decline since 2011, when vacancy rates for purpose-built units came down from above 2 per cent," Urbanation said.

"In fact, it would now take an 82-per-cent increase in vacant units to bring the purpose-built rate back to its 20-year average of 2.1 per cent and the condo vacancy rate up to its 10-year average of 1.1 per cent."

Read more

Growth slows, jobs surprise

Economic growth in Canada is slowing, as expected, but, as Statistics Canada reports, the jobs market is absolutely on fire.

Gross domestic product expanded in the third quarter at a slower annual pace of 1.7 per cent, the federal agency said today. That's pretty much bang on what economists had expected after an exceptionally strong first half of the year.

"Canadian growth was always poised to cool after a monster first half, and the 1.7-per-cent pace in Q3 won't surprise anyone," said Nick Exarhos of CIBC World Markets.

"The details of the GDP report were also broadly as expected, with consumption providing some of the offset to what was a very anemic performance in real exports."

It's today's jobs report that's no doubt raising eyebrows, given that it shows job creation of a stunning 80,000 in November.

The jobless rate declined 0.4 of a percentage point to 5.9 per cent, the lowest since early 2008.

Over the course of 12 months, Statistics Canada said, employment has climbed 2.1 per cent, or by 390,000 positions, all of them full-time.

These monthly reports frequently raise questions among economists given their volatility.

"With strength concentrated in full-time work, there is little doubt that the economy is operating at full capacity and pushing into excess demand territory," said Toronto-Dominion Bank senior economist James Marple.

"This notion is corroborated by the acceleration in wage growth. It's hard to fathom that just a few months ago analysts (ourselves included) were decrying its weakness. The path up from its nadir of 0.6 per cent in April has been rocket-like."

Analysts also cited what this could mean for the Bank of Canada, which is now in pause mode after two rate hikes earlier this year.

"Risks to the outlook notwithstanding, the broad-based strength in jobs and wage growth suggest that the Bank of Canada should continue to normalize monetary policy," Mr. Marple said.

"The Bank of Canada may choose to hold off next week, but the next rate hike is likely not more than a few months away."

The reports sent the Canadian dollar above 78 cents (U.S.).

Read more

- David Parkinson: Economy cools in third quarter

- Josh O’Kane: Unemployment rate falls to lowest since 2008

National Bank raises dividend

National Bank of Canada posted a stronger fourth-quarter profit and, unlike its peers so far this quarter, raised its dividend.

National's profit climbed to $525-million, or $1.39 a share, diluted, from $307-million or 78 cents a year earlier.

The bank also boasted of a record annual profit of $2-billion or $5.38.

It raised its quarterly dividend 3 per cent to 60 cents.

Read more

Markets at a glance

Read more

A ‘leaderless’ Europe

Europe appears on the cusp of a political void that could spell trouble for its fragile economic recovery.

German Chancellor Angela Merkel is on the ropes, which means "a leaderless Europe" amid a host of other issues, National Bank of Canada geopolitical analyst Angelo Katsoras warns.

German Chancellor Angela Merkel holds a news conference after a Eastern Partnership summit at the European Council headquarters in Brussels, Belgium, Nov. 24, 2017.

ERIC VIDAL/REUTERS

"Regardless of the outcome of current negotiations to form a new government, a Germany preoccupied by its increasingly fragmented political landscape has less political capital to dedicate to solving Europe's challenges," Mr. Katsoras said.

"The fact that no other EU member state can step in to fully take over Germany's traditional leadership role further complicates matters," he added in a report.

"Despite France's best efforts to claim this mantle, [President Emmanuel] Macron is dealing with the challenges of converting his economic reforms into stronger growth and is already facing a drop in popularity. Italy is struggling with an economy that has barely grown since it joined the euro zone in 1999 and Spain is more than preoccupied with Catalonia."

The euro zone economies are recovering, but at different paces, and unemployment remains high at 8.8 per cent, with more than 14 million people still looking for work.

To drive home the point, Germany boasts among the lowest of the region's jobless rates, at just 3.6 per cent.

Germany is the euro zone's strongest economy, with Ms. Merkel at the forefront, leading the charge for growth and discipline among member states. Its economy expanded by 0.8 per cent in the third quarter from the second, compared with the euro zone's 0.6 per cent.

But the latest election has left her struggling, and scrambling to put together a coalition.

"Over 20 per cent of the seats in the Bundestag, Germany's parliament, are now held by the two parties on the far right and left of the political spectrum," Mr. Katsoras said, referring to the rightist Alternative for Germany, or AFD, and the aptly-named The Left.

"Both rode a wave of public discontent over migration and/or globalization."

Mr. Katsoras has three scenarios for how it plays out: Dissolution of parliament and new elections, formation of a minority government, or another "grand coalition." The latter, with Ms. Merkel at the helm, is his bet.

"While this could stabilize Germany's political landscape over the short term, the unintended long-term consequence of this strategy could be a further increase in support for formerly marginal forces," Mr. Katsoras said.

"Whatever the outcome, Germany faces weeks, if not months, of inaction," he added.

"The acting government is unlikely to make any major policy decisions at home or the European front. As for Merkel's prospects, while she will probably lead the next government, it is increasingly likely that she will retire from the political scene within the next year or two."

The potential consequences are many.

Given that immigration was such a concern in Germany, the country will now be "even more reluctant" to financially aid other euro zone members, Mr. Katsoras said.

Added to that is the fact that Mr. Macron wants to establish a euro zone financial ministry that would help weaker states, but Germany's political turmoil is getting in the way of that.

France’s President Emmanuel Macron attends an award ceremony in the courtyard of the Invalides, in Paris, Monday, Nov. 27, 2017.

THIBAULT CAMUS/THE ASSOCIATED PRESS

"Convincing Germany that it should be even more financially liable for the spending decisions of other countries would have been very difficult under the best of circumstances," Mr. Katsoras said.

"Under Germany's current domestic political situation, it is near impossible. The Netherlands, Finland and Austria are also strongly opposed to providing great financial support to other countries. Macron's positions have led the German press to refer to him as a ' teurer freund,' which is German for 'expensive friend.'"

There's also the threat of holding up Brexit trade negotiations.

And while the euro zone is rebounding, support for far right and left politicians is growing.

"The challenge of containing these forces would be even more difficult if Europe entered an economic downturn," Mr. Katsoras said.

Read more

- Merkel’s conservative party agrees to pursue grand coalition in Germany

- Euro zone business roars as Germany leads the pride