Bristol Myers Squibb(NYSE: BMY) is one of the largest healthcare companies in the world. It has faced adversity throughout the years, but it still managed to continually find ways to grow and diversify its business.

The current adversity comes from investors worrying about its top-selling drug Revlimid and other products losing market share. But Bristol Myers' recent quarterly results demonstrate exactly why investors shouldn't be overly concerned about the business.

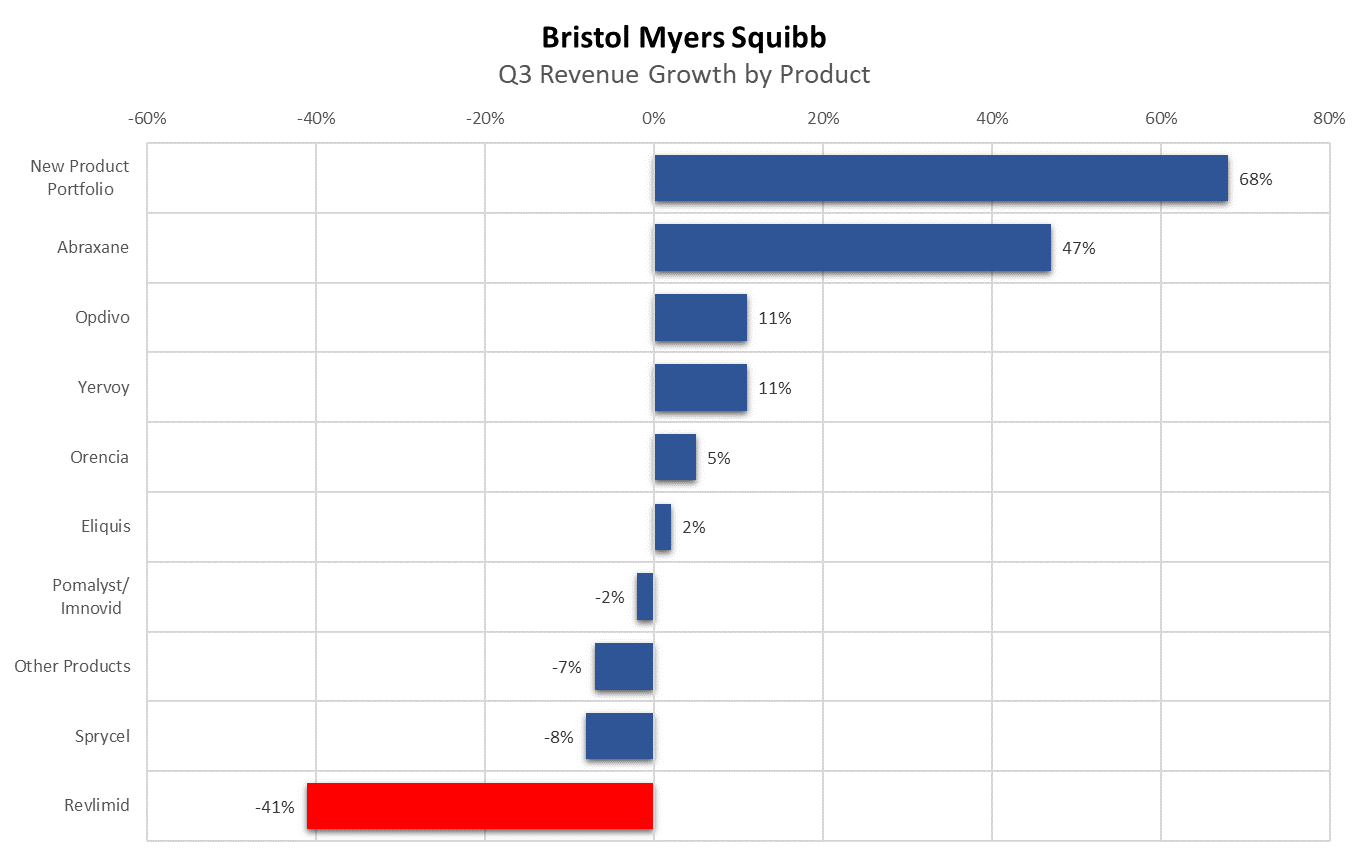

Revlimid crashed by 41%, but overall earnings didn't tank

Bristol Myers' cancer drug Revlimid has been one of its key assets over the years. But with a loss in patent protection and rising competition, its sales have been falling. In the company's third-quarter earnings report, Revlimid's sales totaled $1.4 billion which represented a 41% year-over-year drop.

Image source: Company filings.

Revlimid remains one of the company's top-selling drugs, although cancer drug Opdivo and blood clot medication Eliquis are firmly ahead at this point. As recently as 2021, Revlimid was still the company's top-selling product, so the fact that not one but two drugs are now ahead of it is a significant change in Bristol Myers' operations.

What's also encouraging is that Bristol Myers' bottom line was actually higher this past quarter than it was a year ago. Net earnings of $1.9 billion rose 20% year over year due to a decline in operating expenses and a fairly resilient top line that only fell by 2%. And that's because the company has many other fast-growing products in its portfolio.

New products drive a lot of the growth

Bristol Myers has been investing in strengthening its top line through both acquisitions and spending on research and development. And it does appear to be paying off. Management projects that the company's new product portfolio will be able to generate $10 billion in revenue by 2026. By 2029, that number could reach $25 billion.

Last quarter, its new products were a key reason why the top line didn't fall much further down than it did, and thus enabled the bottom line to remain strong.

Image source: Company filings.

A couple of particularly high performers in its new product portfolio were cancer drug Opdualag, whose sales rose by 98%, and Zeposia, which treats relapsing multiple sclerosis, with its revenue growing by 78%. Even as those growth rates inevitably slow down, it appears to be only a matter of time before the company's portfolio of new products overtakes Revlimid in sales, further lessening its dependence on the drug.

There's still risk with Bristol Myers

Although this past quarter was encouraging for Bristol Myers, the company isn't out of the woods by any stretch. Top-selling drugs Eliquis and Opdivo face their own patent cliffs this decade. Plus, Bristol Myers has a mountain of long-term debt, which totals more than $32 billion. The company has trimmed that from the more than $35 billion it reported at the end of last year. However, it's still a sizable amount to be carrying, particularly as interest rates remain high.

Why Bristol Myers is a good buy

Bristol Myers isn't a risk-free investment, but the stock isn't nearly as dangerous as its incredibly low forward price-to-earnings multiple of 7 seems to suggest. Investors appear to be discounting the stock excessively, which looks to be a mistake. The healthcare company is finding ways to grow its business, and while it is facing patent cliffs, it still has time to bridge those gaps.

With strong financials, it can continue to pay down its debt while also investing in its pipeline. And if worse comes to worst, it could slow the pace of its dividend hikes or even reduce its payouts altogether. Either way, this is by no means a broken business, and while it is facing some challenges right now, Bristol Myers can make for an underrated investment if you're willing to hang on for the long term.

10 stocks we like better than Bristol Myers Squibb

When our analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and Bristol Myers Squibb wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of November 6, 2023

David Jagielski has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Bristol Myers Squibb. The Motley Fool has a disclosure policy.