2 Stocks With 4.0%+ Yields and Growing Earnings and Dividends

These two stocks have growing earnings and dividends and have dividend yields of over 4.0%. Moreover, there are interesting ways to play them with options. The two are Fidelity National Financial (FNF), a real estate title insurance and escrow company, and Carter's Inc. (CRI), a maker of baby and infant clothing.

Fidelity National Financial (FCF)

This title, escrow, and trust company will post slightly lower revenue but higher earnings-per-share growth by 2023. FNF stock is off 28.3% YTD as of mid-day on June 29. At $36.85 with its $1.76 dividend per share (DPS), the stock has a dividend yield of 4.78%.

This gives this undervalued stock a cheap 6.1x earnings multiple as 6 analysts surveyed by Seeking Alpha have an average earnings per share (EPS) estimate of $6.02. As it stands now these analysts are projecting higher EPS at $6.19 for 2023.

Moreover, the dividend payout ratio is very low since the $1.76 annual dividend represents just 29.2% of its earnings estimate for 2022. That should give investors a good deal of comfort that the dividend will be able to be paid even if a severe recession hits.

Moreover, Fidelity National has paid its dividends every year for the past 16 years, and for the past 7 years has raised its dividends every year. Moreover, the average price target for these 6 analysts is $56.00 per share, or 52% over today's price.

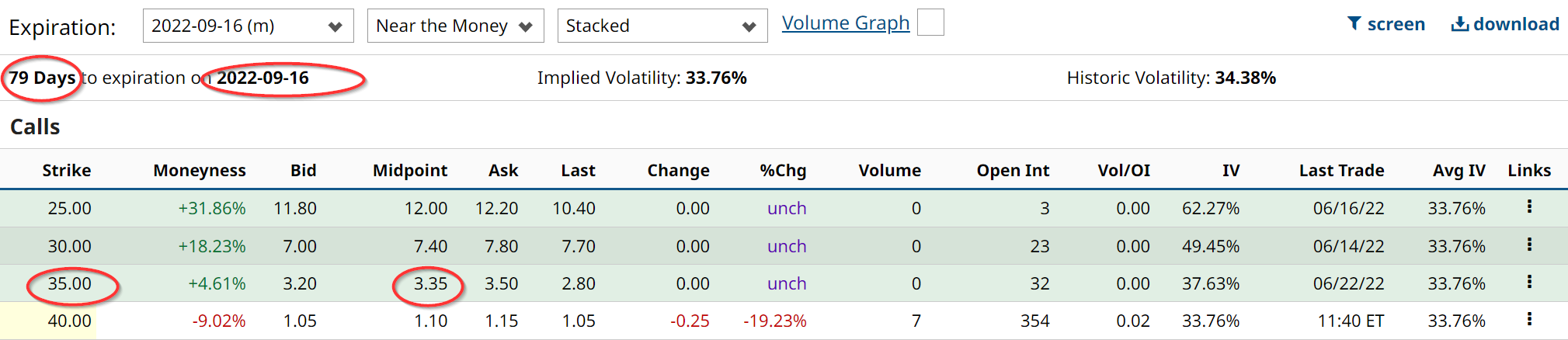

One way to play this is to buy the 3 months out $35 calls for $3.35. as an in-the-money purchase. You can see this in the Barchart option chain below:

This shows that the Sept. 16 calls at $35 will cost $3.35 in the mid-point, so the all-in cost if held till expiration and exercised, will be $38.35. That is just 1.04% over today's price of $36.85, but provides 11x leverage to the investor. This is because the stock price of $36.85 is exactly 11 times the option premium cost of $3.35.

Therefore even a small move up in the stock price will be leveraged 11x in your call price investment. And, of course, the downside risk is just as great. Except for one thing. The huge dividend yield tends to ameliorate large downside activity. In addition, the company's buybacks will help push the stock higher. Last quarter it spent $134 million on buybacks or about 5% of its $10.54 billion market cap on an annualized basis.

Carter's Inc (CRI)

This baby and infant clothing retailer is very popular. Earnings are still forecast to grow 9.6% next year at $9.80 per share, putting it on a forward 8x P/E this year and 7.3 P/E multiple for 2023.

Its $3.00 per share dividend is well covered by earnings and provides a 4.25% dividend yield. In addition, it has a large $250 million buyback program which works out to 4.3% of its $5.8 billion market capitalization. Analysts have an average target price of $104 per share, or over 47% higher than its price of $70.65 today.

One way to play this is to buy 3-month forward $75 strike price calls.

The table above shows that at the midpoint the Sept. 16 calls at $75 strike price cost $3.50. That means that the all-in cost, if held til expiration and exercised would cost $78.50, or 11.1% over today's price. The stock needs to rise by 11% just for these calls to be at breakeven.

The $70 calls cost $5.75 and represent an all-in cost of $75.75, or 7.2% over today's price. That is a more conservative way to play the upside since as the stock rises to $75.75 a higher percentage of the price is in the money. Either call option provides a huge upside if the stock rises to $104 price target that analysts are looking for.

More Stock Market News from Barchart

Provided Content: Content provided by Barchart. The Globe and Mail was not involved, and material was not reviewed prior to publication.