Bailey McLean/The Globe and Mail

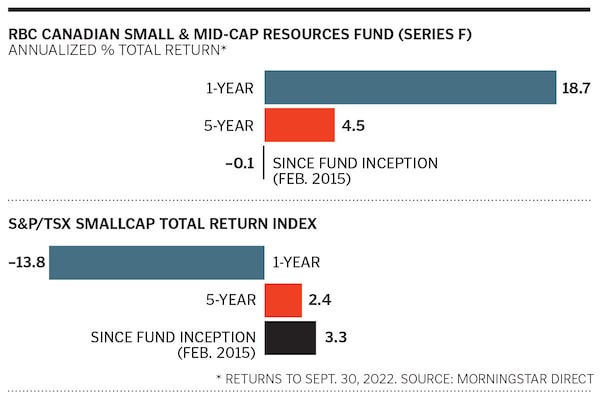

Brahm Spilfogel sees running the RBC Canadian Small & Mid-Cap Resources Fund on top of a larger-company resource portfolio as having a competitive edge. He can gain insight into smaller companies that might graduate to the RBC Global Resources Fund or get swallowed by bigger firms. Tracking a broad spectrum of companies also helps him find the best management teams—key for investing in resource stocks. Over the past five years, the $375-million smaller-cap fund, which he co-manages with Chris Beer, has also outpaced the S&P/TSX SmallCap Index, including dividends. We asked Spilfogel, 53, why the energy sector is in a sweet spot and what makes uranium junior NexGen Energy attractive.

What is your outlook for resources?

We are cautious on energy and materials for the next three to six months because we expect a global recession. The Russia-Ukraine war has put a strain on industrial activity in Europe. Central banks are raising interest rates to slow inflation. And China’s COVID-19 lockdowns don’t help resource demand. Longer term, once the U.S. dollar has peaked and interest rates start to fall, the set-up for energy and materials is very bullish. Both sectors have survived a very difficult last decade, and balance sheets have recovered and are strong.

Why are you bullish on oil stocks this decade?

We are seeing disciplined production growth, not only with the Organization of Petroleum Exporting Countries, but also with most North American and European producers. Capital expenditures are 40% lower than we think is needed for medium-term demand projections. Once the economy rebounds, we could have a tight oil market for years. We have raised our long-term expectations for oil from US$60 per barrel for West Texas Intermediate crude to US$80, but it could reach US$150 in very tight markets. Valuations for energy stocks are very attractive. We like names like Meg Energy as well as Enerplus, which has done a good job of acquiring assets at the bottom of the cycle.

What about natural gas?

Longer term, I really like this sector. We see more manufacturing returning to the U.S., which will drive industrial gas demand, and U.S. liquefied natural gas export capacity doubling by 2030. I think the Henry Hub natural gas price will trade at over US$3 per million British thermal units for the rest of the decade, whereas it has been below that price for the last five years. We like Tourmaline Oil and Arc Resources. They have long-life assets, are low-cost producers and have good management teams.

NexGen Energy is a top holding. What’s the attraction?

China’s ambition to grow its nuclear generation to more than 100 gigawatts by the end of the decade is driving global uranium demand. Nuclear power has become a green option because it doesn’t create CO2. Rather than winding down existing nuclear fleets, there is a growing understanding that combining baseload nuclear power with variable wind and solar renewable power production is needed to stabilize the electric grid. NexGen’s Arrow deposit is poised to be one of the next decade’s new primary sources of uranium supply.

How else are you playing the energy transition?

A copper shortage is expected post 2025. The metal is needed for wind and solar technologies, power-distribution lines and electric vehicle chargers. Europe’s emissions-reduction target for 2030 will add 4% to annual global copper demand, while China and U.S. will require more, too. Copper producer Ivanhoe Mines is a top holding. Lithium demand driven by EV growth is expected to grow 100% over the next few years, but the projected supply is uncertain. We own a couple of lithium juniors, including Lithium Americas.

What is your outlook for lumber?

With 30-year U.S. mortgage rates at around 7%, housing starts will remain under pressure. But interest rates are going to come down at some point, and people will return to buying new or existing houses. The chronic shortage of housing in North America will drive this sector for the coming decade. Lumber companies have great balance sheets with little or no debt. We own West Fraser Timber Co., Canfor and Interfor in this space.

The Globe and Mail

Your time is valuable. Have the Top Business Headlines newsletter conveniently delivered to your inbox in the morning or evening. Sign up today.