Lovesac (NASDAQ:LOVE) Reports Sales Below Analyst Estimates In Q4 Earnings, Stock Drops 18.6%

Furniture company Lovesac (NASDAQ:LOVE) fell short of analysts' expectations in Q4 CY2023, with revenue up 4.9% year on year to $250.5 million. Next quarter's revenue guidance of $129 million also underwhelmed, coming in 13.8% below analysts' estimates. It made a GAAP profit of $1.87 per share, improving from its profit of $1.74 per share in the same quarter last year.

Is now the time to buy Lovesac? Find out by accessing our full research report, it's free.

Lovesac (LOVE) Q4 CY2023 Highlights:

- Revenue: $250.5 million vs analyst estimates of $265.4 million (5.6% miss)

- EPS: $1.87 vs analyst expectations of $1.93 (2.9% miss)

- Revenue Guidance for Q1 CY2024 is $129 million at the midpoint, below analyst estimates of $149.6 million (EPS guidance for the period missed meaningfully)

- Management's revenue guidance for the upcoming financial year 2025 is $735 million at the midpoint, missing analyst estimates by 4.7% and implying 5% growth (vs 8.1% in FY2024) (EPS guidance for the period missed meaningfully)

- Gross Margin (GAAP): 59.7%, up from 56.6% in the same quarter last year

- Market Capitalization: $361.5 million

Shawn Nelson, Chief Executive Officer, stated, “Lovesac delivered market leading fiscal fourth quarter and full year 2024 sales performances. We surpassed $700 million in revenues for the fiscal year, representing a net sales increase of $49.1 million, or 7.5%, despite another year of significant category decline for the home furnishing sector. Interest in – and passion for – the Lovesac brand, from new and existing customers alike, continues to grow. We will fortify our momentum by doubling-down on what we do best: strengthening our unique omni-channel infinity flywheel, reinforcing our designed for life platform, investing in genuine innovation, and making the strategic investments necessary to profitably scale our brand and business for years to come.”

Known for its oversized, premium beanbags, Lovesac (NASDAQ:LOVE) is a specialty furniture brand selling modular furniture.

Home Furnishings

A healthy housing market is good for furniture demand as more consumers are buying, renting, moving, and renovating. On the other hand, periods of economic weakness or high interest rates discourage home sales and can squelch demand. In addition, home furnishing companies must contend with shifting consumer preferences such as the growing propensity to buy goods online, including big things like mattresses and sofas that were once thought to be immune from e-commerce competition.

Sales Growth

A company's long-term performance can indicate its business quality. Any business can enjoy short-lived success, but best-in-class ones sustain growth over many years. Lovesac's annualized revenue growth rate of 33.4% over the last five years was incredible for a consumer discretionary business.  Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. Lovesac's recent history shows its momentum has slowed as its annualized revenue growth of 18.6% over the last two years is below its five-year trend.

Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. Lovesac's recent history shows its momentum has slowed as its annualized revenue growth of 18.6% over the last two years is below its five-year trend.

This quarter, Lovesac's revenue grew 4.9% year on year to $250.5 million, falling short of Wall Street's estimates. The company is guiding for a 8.6% year-on-year revenue decline next quarter to $129 million, a reversal from the 9.1% year-on-year increase it recorded in the same quarter last year. Looking ahead, Wall Street expects sales to grow 8.5% over the next 12 months, an acceleration from this quarter.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

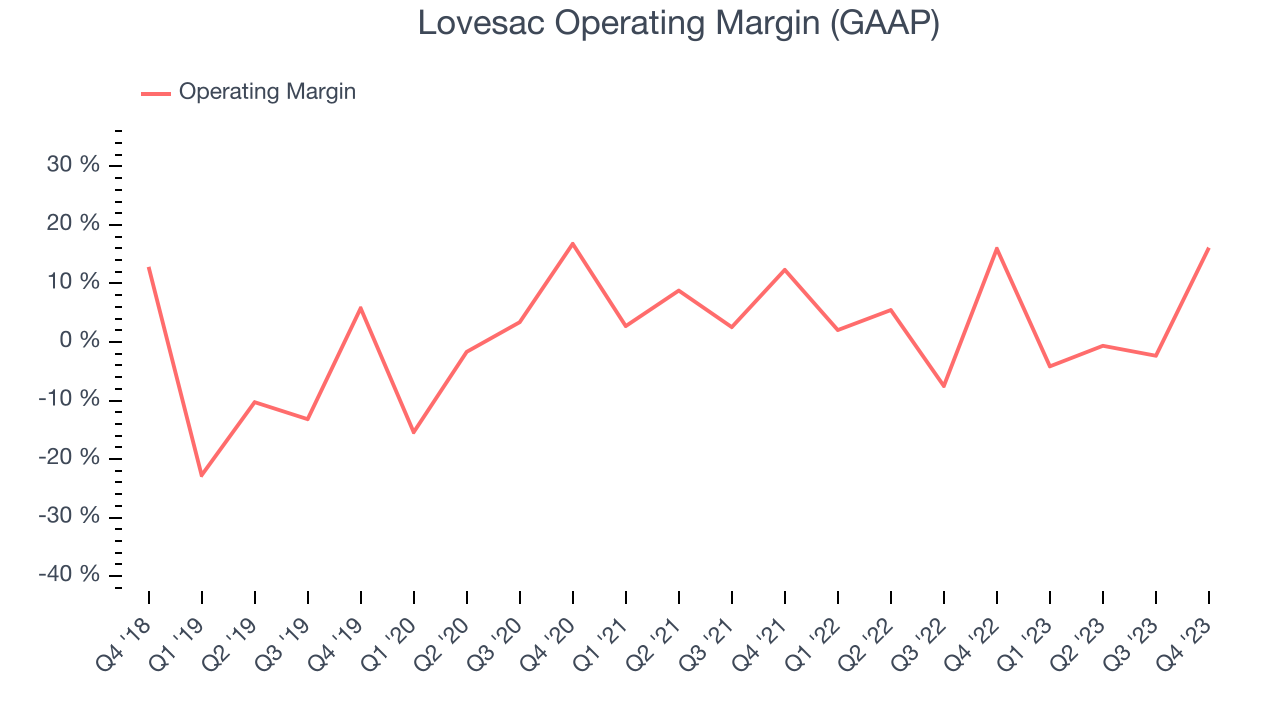

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income–the bottom line–excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Lovesac was profitable over the last eight quarters but held back by its large expense base. It's demonstrated subpar profitability for a consumer discretionary business, producing an average operating margin of 5.1%.

This quarter, Lovesac generated an operating profit margin of 16.1%, in line with the same quarter last year. This indicates the company's costs have been relatively stable.

Over the next 12 months, Wall Street expects Lovesac to become more profitable. Analysts are expecting the company’s LTM operating margin of 4.3% to rise to 5.7%.Key Takeaways from Lovesac's Q4 Results

Revenue and EPS both missed. Guidance wasn't much better. Next quarter's revenue and EPS guidance, as well as the full year outlook for revenue and EPS, missed expectations. In the release, management mentioned that they were anticipating an "eventual category rebound". Overall, this was a bad quarter for Lovesac. The company is down 16.5% on the results and currently trades at $19.47 per share.

Lovesac may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.