The stock's setback last week makes enough sense on the surface. In defiance of expectations, JPMorgan Chase(NYSE: JPM) didn't raise its 2024 revenue guidance with its first-quarter results posted on Friday. Shares subsequently tumbled to the tune of 6%, extending a sell-off that's been underway since late March. JPMorgan stock is now down 8% from that peak.

The proverbial glass isn't half-empty, however. It's half-full. This dip is a great opportunity to jump on one of the financial sector's top stocks at a bargain price. Here's why.

The quarter that was, and the year that won't be

During the three-month stretch ending in March, JPMorgan Chase turned $42.6 billion worth of revenue into a per-share operating profit of $4.44. Both figures were better than estimates of $41.9 billion and $4.11 (respectively). And both were improvements on the year-earlier comparisons of $39.3 billion and $4.10 per share (again, respectively).

The stumbling block was guidance. JPMorgan believes it will be banking on the order of $90 billion worth of net interest income this year, in line with its outlook from just three months earlier. Investors were expecting the company to raise that figure by between $2 billion and $3 billion. When it didn't, the market dished out a mini-revolt.

However, there are some encouraging figures buried in JPMorgan Chase's Q1 numbers that bolster an already bullish case.

JPMorgan Chase still shines

In the simplest terms, this mega-bank is faring far better than most of its peers are at this time.

Take its shrinking losses on loans as an example. Whereas Wells Fargo(NYSE: WFC) and Citigroup(NYSE: C) are both logging measurable growth in their charge-offs and loss provisions, JPMorgan's total allowance for credit losses actually fell just a bit between the fourth quarter of last year and the first quarter of 2024. Charge-offs and delinquencies were up just a little last quarter, but only a little, and the bulk of that growth came from its credit card business. Moreover, its total credit-loss-allowance-to-loan-portfolio ratio has held steady for the past year.

It's also worth noting that -- despite the bank's unwillingness to raise its previous net interest income guidance for 2024 -- JPMorgan Chase's interest income did grow year over year last quarter, from $20.7 billion to $23.1 billion. Citigroup's net interest income was only up by 1%, while Wells Fargo's net interest income fell 8% on a year-over-year basis.

Also keep in mind that while JPMorgan Chase didn't raise its interest income outlook for the current fiscal year, its expectation of around $90 billion worth of net interest income for 2024 is still slightly better than 2023's tally. Growth on other fronts, meanwhile, should offset any slowdown in interest rate income growth.

On that note, after a fairly challenging 2023 for most of the bank's businesses, a handful of green shoots started popping up during Q1. Investment banking fees improved 18% versus the year-earlier figure, for example, and were up 20% from the fourth quarter's tally. Wealth management revenue and even lending-based fee income were up comparably.

This measurable growth precedes what could be a robust recovery of the capital markets and corporate fundraising business in the latter half of 2024. In the meantime, the Federal Reserve reports that the banking industry as a whole is anticipating increased demand for new loans this year, driven by eventual interest rate cuts.

It really is a fortress balance sheet, and it matters

Then there's the even-less-obvious stuff, like JPMorgan's healthy balance sheet and its subsequently strong efficiency measures.

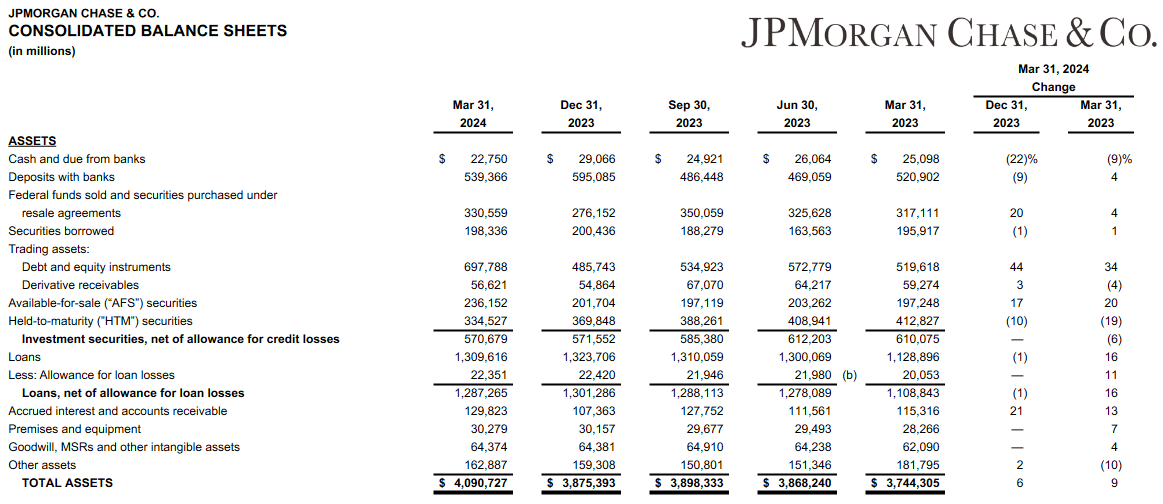

Remember last year's meltdown of SVB Financial's Silicon Valley Bank and First Republic Bank? At the heart of their liquidity issues were too many long-term interest-bearing assets meant to be held for a long time ("held to maturity," or "HTM"), and too few short-term interest-bearing securities that could have been sold quickly ("available for sale," or "AFS"). Most banks own both kinds. The key is just finding the right, balanced proportion of the two. Silicon Valley Bank and First Republic Bank didn't.

To its credit, JPMorgan Chase was never in any real liquidity jeopardy ... then, or now. Nevertheless, the bank has been able to dial back its less-liquid HTM holdings and ramp up its AFS securities. This provides the bank with a much higher degree of fiscal flexibility, should the need arise.

Image source: JPMorgan Chase Q1-2024 earnings supplement.

In this same vein, what the company refers to as its "fortress balance sheet" is currently capable of surviving $520 billion worth of losses without breaking the bank, so to speak.

There's more to the story than just having enough liquid assets at its disposal, though. The rock-solid balance sheet ultimately translates into more efficient, more profitable use of these assets. JPMorgan's return on its total equity (ROE) stands at 17% as of Q1, while the return on its tangible common equity (ROTCE) reached 21% for the recently ended quarter. For comparison, Wells Fargo's ROE fell to 10.5% during Q1, while its ROTCE slipped from 14% a year earlier to 12.3% last quarter. Citi's comparable numbers for the quarter in question are 6.6% and 7.6%, respectively.

JPMorgan Chase stock is a best-of-breed pick worth buying now

Companies are more than mere numbers, of course. Like people and pets, they each have their own personality. That can make a difference in their stocks' performance. JPMorgan is no exception to this reality.

Nevertheless, truly great companies consistently produce objectively healthy fiscal results. JPMorgan Chase has been doing exactly that for years, and it still is.

Take the hint. This is one of the financial sector's strongest names, if not its strongest. The stock's post-earnings dip is a buying opportunity, even if the exact bottom has not been hit yet. You'll be stepping in while shares are priced at roughly 12 times this year's projected earnings, and while it's yielding a little more than 2.3%.

Should you invest $1,000 in JPMorgan Chase right now?

Before you buy stock in JPMorgan Chase, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and JPMorgan Chase wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of April 8, 2024

Citigroup is an advertising partner of The Ascent, a Motley Fool company. SVB Financial provides credit and banking services to The Motley Fool. Wells Fargo is an advertising partner of The Ascent, a Motley Fool company. JPMorgan Chase is an advertising partner of The Ascent, a Motley Fool company. James Brumley has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends JPMorgan Chase. The Motley Fool has a disclosure policy.