Williams-Sonoma's (NYSE:WSM) Q4 Sales Beat Estimates

Kitchenware and home goods retailer Williams-Sonoma (NYSE:WSM) reported Q4 FY2023 results topping analysts' expectations, with revenue down 7.1% year on year to $2.28 billion. It made a non-GAAP profit of $5.44 per share, down from its profit of $5.50 per share in the same quarter last year.

Is now the time to buy Williams-Sonoma? Find out by accessing our full research report, it's free.

Williams-Sonoma (WSM) Q4 FY2023 Highlights:

- Revenue: $2.28 billion vs analyst estimates of $2.23 billion (2.4% beat)

- EPS (non-GAAP): $5.44 vs analyst estimates of $5.16 (5.5% beat)

- Gross Margin (GAAP): 46%, up from 41.2% in the same quarter last year

- Same-Store Sales were down 6.8% year on year

- Store Locations: 518 at quarter end, decreasing by 12 over the last 12 months

- Market Capitalization: $15.46 billion

“We are pleased with our strong finish to 2023. We delivered an annual operating margin of 16.4% with full-year earnings per share of $14.85, beating our 2023 comp guidance of -10% to -12% and hitting our operating margin range of 16% to 16.5%,” said Laura Alber, President and Chief Executive Officer.

Started in 1956 as a store specializing in French cookware, Williams-Sonoma (NYSE:WSM) is a specialty retailer of higher-end kitchenware, home goods, and furniture.

Home Furniture Retailer

Furniture retailers understand that ‘home is where the heart is’ but that no home is complete without that comfy sofa to kick back on or a dreamy bed to rest in. These stores focus on providing not only what is practically needed in a house but also aesthetics, style, and charm in the form of tables, lamps, and mirrors. Decades ago, it was thought that furniture would resist e-commerce because of the logistical challenges of shipping large furniture, but now you can buy a mattress online and get it in a box a few days later; so just like other retailers, furniture stores need to adapt to new realities and consumer behaviors.

Sales Growth

Williams-Sonoma is larger than most consumer retail companies and benefits from economies of scale, giving it an edge over its competitors.

As you can see below, the company's annualized revenue growth rate of 7.1% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was weak despite closing stores.

This quarter, Williams-Sonoma's revenue fell 7.1% year on year to $2.28 billion but beat Wall Street's estimates by 2.4%. Looking ahead, Wall Street expects revenue to decline 2.1% over the next 12 months.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

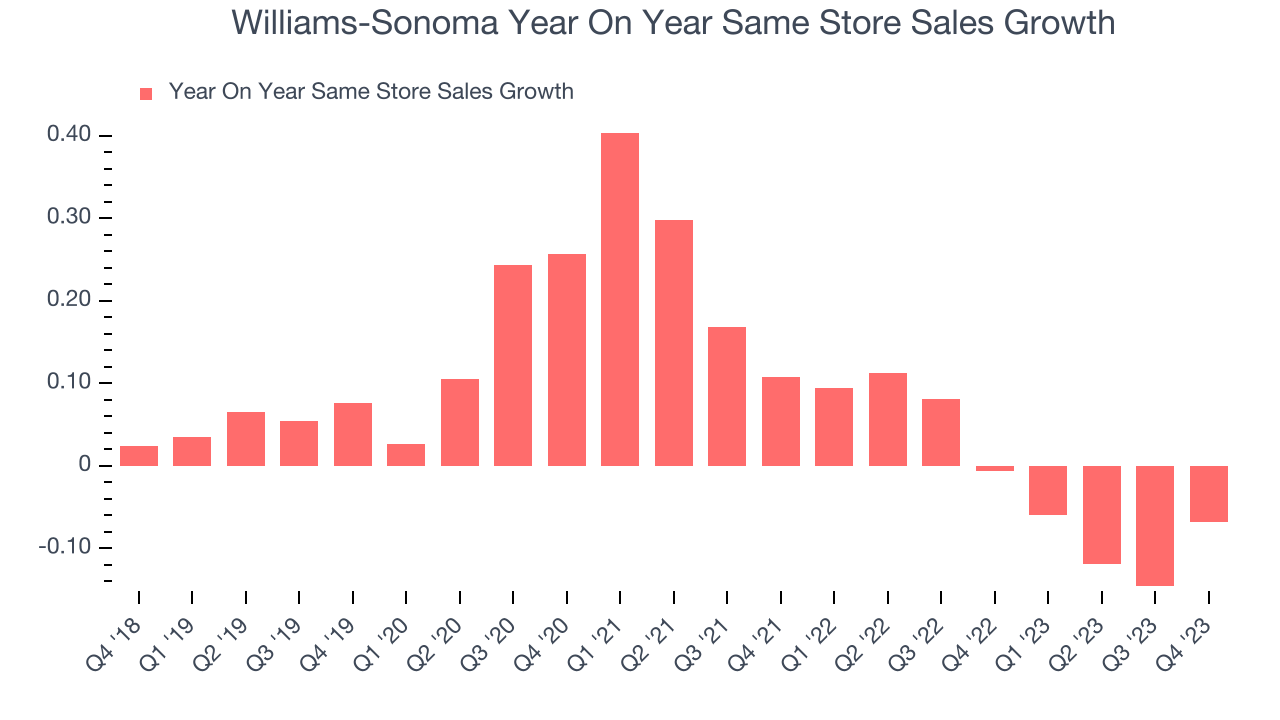

Same-Store Sales

A company's same-store sales growth shows the year-on-year change in sales for its brick-and-mortar stores that have been open for at least a year, give or take, and e-commerce platform. This is a key performance indicator for retailers because it measures organic growth and demand.

Williams-Sonoma's demand has been shrinking over the last eight quarters, and on average, its same-store sales have declined by 1.4% year on year. The company has been reducing its store count as fewer locations sometimes lead to higher same-store sales, but that hasn't been the case here.

In the latest quarter, Williams-Sonoma's same-store sales fell 6.8% year on year. This decrease was a further deceleration from the 0.6% year-on-year decline it posted 12 months ago. We hope the business can get back on track.

Key Takeaways from Williams-Sonoma's Q4 Results

We enjoyed seeing Williams-Sonoma exceed analysts' gross margin expectations this quarter. Management noted that although 2023 was the slowest housing market in several decades, it avoided discounting, enabling it to deliver an operating margin ahead of its pre-pandemic profitability.

We were also excited the company's revenue outperformed Wall Street's estimates, driven by better-than-expected same-store sales at its flagship Williams Sonoma brand (1.6% growth vs estimates of negative 0.5%) and Pottery Barn (negative 9.6% vs estimates of negative 10.3%). The revenue and gross margin beats also led to an EPS beat, and management increased the company's quarterly dividend by 26% and share repurchase capacity to $1 billion. Zooming out, we think this was a great quarter that shareholders will appreciate. The stock is up 4.9% after reporting and currently trades at $253 per share.

Williams-Sonoma may have had a good quarter, but does that mean you should invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.