This Undervalued Energy Stock Could Rally 20%

Oil prices have pulled back significantly from their September 2023 highs around $95 per barrel, even as crude for March delivery (CLH24) ticks higher today on strong economic data. As a result, many energy stocks have retreated, too - and some are now trading at compelling valuations.

One stock that appears poised for a rally is Valero Energy Corporation (VLO), one of the biggest names in refining - and right now, one of the cheapest. The current valuation gap compared to VLO's peers suggests the shares are priced at a bargain right now. Plus, the company offers a dividend yield exceeding 3%, too.

Let's take a closer look at the stock's combination of value and yield, plus the optimistic price forecasts from analysts.

Is Valero Energy Stock a Bargain Right Now?

San Antonio-based Valero Energy Corporation, valued at $43 billion by market cap, is the largest downstream energy player in the U.S. The company operates in three key segments: Refining, Ethanol, and Renewable Diesel.

VLO's focus on growth in cleaner energy is notable. They're putting 40% of their growth capital into low carbon projects, betting big on things like renewable diesel and sustainable aviation fuel (SAF). The biofuels market is predicted to surge by 20% by 2027, with ethanol leading the charge.

The stock has pulled back roughly 8% over the past 52 weeks, which significantly lags the performance of the broader equities market. For perspective, the S&P 500 Index($SPX), of which VLO is a member, has gained more than 21% over this time frame. That said, the S&P 500 Energy Sector SPDR (XLE) has declined by a steeper 10.4%.

Following its lackluster share price performance over the past year, the stock is a relatively compelling value. VLO is priced at a forward earnings multiple of 5.19x, which is well below the energy sector median of 9.64x. Likewise, at 0.29x forward sales, VLO is priced at a steep discount to its sector peers - and the stock's price/cash flow ratio of 4.02 is also a bargain compared to the 4.56 sector median.

These multiples are not only lower than most of Valero's energy sector competitors, they're also lower than the stock's own five-year averages for these valuation metrics. In other words, VLO is cheap at current levels.

Valero Energy's Financial Performance

Valero's most recent Q3 2023 earnings beat expectations, with EPS of $7.49 topping analysts' estimates - even as revenue fell short of the consensus.

In terms of cash, Valero ended the quarter with a cash position of $5.8 billion, with adjusted net cash from operating activities arriving at $3.2 billion for Q3. The debt to capitalization ratio was 17%.

Analysts have set the bar relatively low for Valero in the upcoming fiscal year, with Wall Street targeting an EPS decline of 39% to $14.80 in FY 2024, with revenue projected to drop 3% to $141.31 billion. Valero Energy is expected to report earnings again on Jan. 25.

VLO Pays Back Shareholders

Right now, VLO offers a forward dividend yield of 3.23%. That's not necessarily the highest yield in the energy sector, but it's more generous than peers than like Murphy USA (MUSA) and Marathon Petroleum (MPC).

The company targets an annual payout ratio between 40-50% of adjusted net cash provided by operating activities, but surpassed that mark with a Q3 payout ratio of 68%. In total, Valero paid out $360 million in dividends during the third quarter, and repurchased 13 million shares of common stock worth $1.8 billion.

Looking back, Valero has raised its quarterly dividend consistently for 11 years. Given the company's strong cash position and commitment to paying back shareholders, additional dividend increases seem likely.

What Do Analysts Expect for VLO?

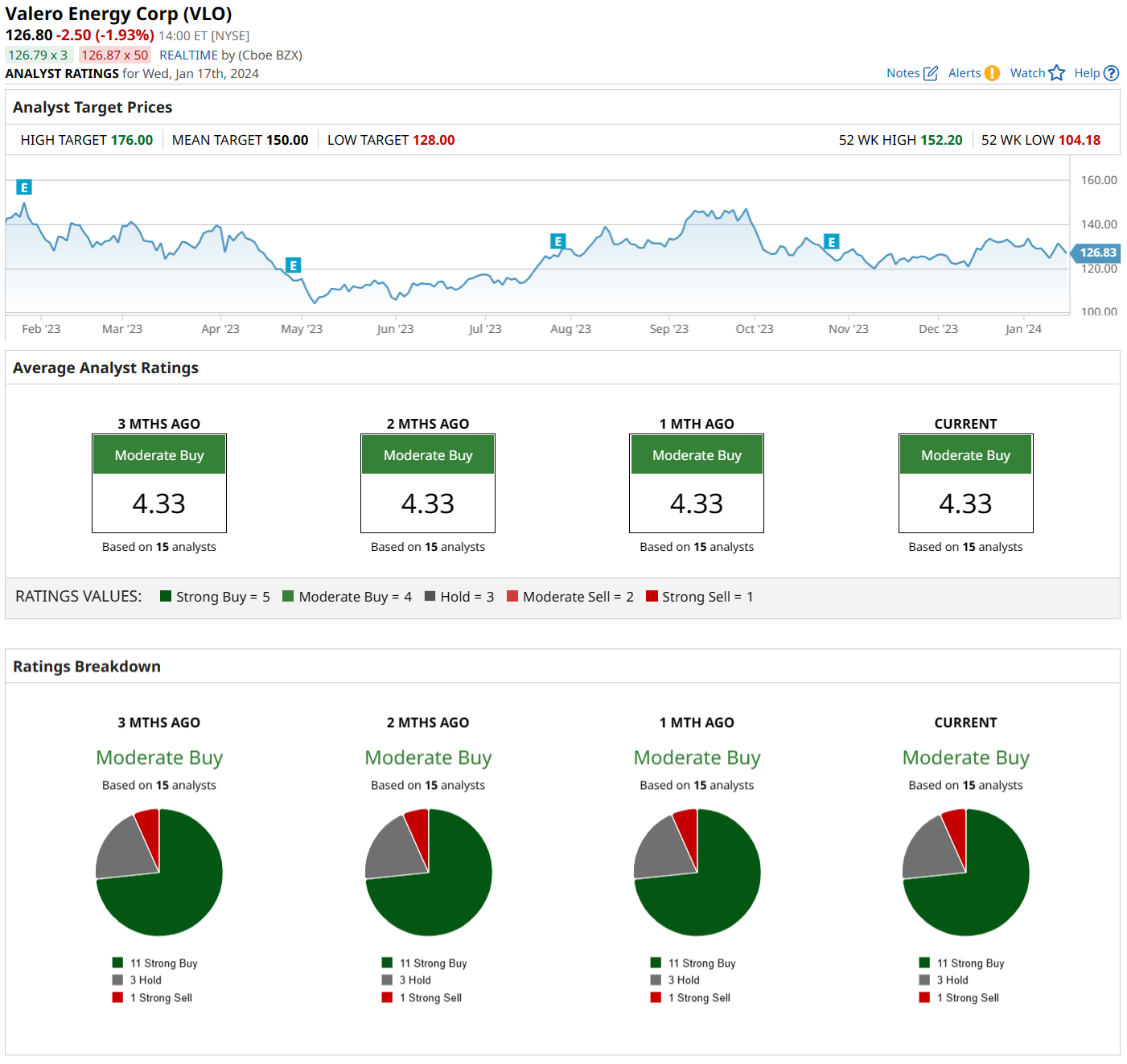

Analysts are upbeat about VLO's prospects, with the average target price set at $150.00 - indicating a potential 20% upside from current levels.

The consensus rating is a “moderate buy,” with a whopping 11 analysts giving it a “strong buy,” 3 suggesting a “hold,” and only 1 daring to say it's a “strong sell.”

Conclusion

Valero Energy Corporation (VLO) seems to be a top value pick in the energy sector, with the shares poised for a potential 20% rally. In light of its historically low valuations, diverse energy portfolio, and solid cash position, it's worth considering the shares right now while they're cheap.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.