Real estate investment trusts (REITs) have sold off this year due to concerns about a recession as interest rates head higher. That has investors worried about their near-term growth prospects.

However, while the market is focusing on the short term, several REITs are benefiting from major long-term growth drivers that remain firmly in place. Three that stand out to our contributors are Alexandria Real Estate Equities(NYSE: ARE), Crown Castle International (NYSE: CCI), and Prologis (NYSE: PLD). Here's why they think dividend investors should scoop up these REITs -- which now offer even higher dividend yields -- before the market realizes that they have a lot of growth ahead.

An office REIT that focuses on life sciences

Brent Nyitray (Alexandria Real Estate Equities): Office real estate investment trusts (REITs) have been under a cloud since the COVID-19 pandemic proved that the work-from-home model is a legitimate and effective way for companies to conduct business. Employees generally love the idea, although employers have been less enamored with the model. That said, not all industries are well-suited for a work-from-home model, and this is where Alexandria comes in.

Alexandria focuses on two types of companies: High-tech and life sciences. Its biggest tenants are life sciences companies like Bristol-Myers Squibb, Moderna, and Illumina. Other big tenants include the U.S. government and Uber Technologies. Life sciences companies generally require sophisticated laboratory spaces, and these companies generally aren't conducive to the work-from-home model.

Alexandria was the first-mover in the life sciences space, and it is difficult for a new entrant to compete given that Alexandria has a long track record of working with these companies and the regulators who set many of the requirements.

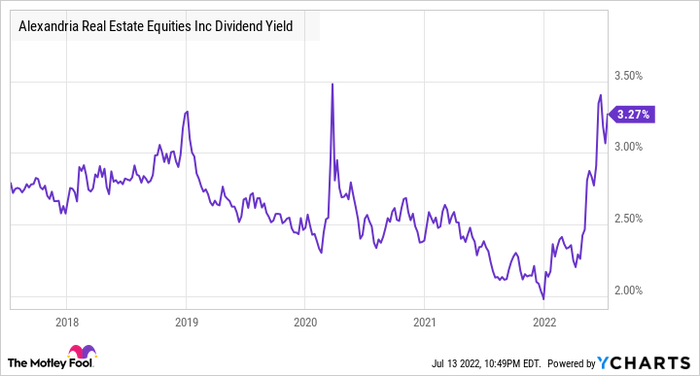

Alexandria has been beaten up so far this year, as REITs have been under a cloud. It did disappoint on its first-quarter numbers; however, it recently hiked its dividend. Much of the lousy sentiment is due to the increase in interest rates as REITs often trade on dividend yields. Alexandria is trading with a 3.3% dividend yield, which is toward the highs of the past five years.

ARE Dividend Yield data by YCharts

Alexandria will continue to benefit from increased spending on research and development in the life sciences space, and is the market leader in life sciences office space.

This tower titan is transitioning to small cells

Marc Rapport (Crown Castle International): Crown Castle International stock has fallen along with the market and is now down about 19% year to date. This seems like a buying opportunity, for three good reasons.

First, the Houston-based company has built an impressive record of investor returns. It built and leased mobile cell towers, benefiting from the growth of this industry (and the major carriers that depend on this infrastructure). Crown Castle opened for business in 1994 with 133 towers, went public in 1998 with about 1,400 of them, and now has more than 40,000. Since that IPO, this stock has more than tripled the total return of the S&P 500, turning a $10,000 investment into about $177,000.

Second, Crown Castle says tower space application activity remains strong while the company simultaneously moves forward aggressively on the rollout of small cell nodes and other data storage and distribution technologies that support next-generation wireless capabilities.

Company CEO Jay Brown says 2022 is "an important transition year" as Crown Castle begins adding small cell nodes at a pace expected to reach 10,000 a year by next year. It already has about 115,000 of them on air or in the backlog and more than 80,000 miles of installed fiber optic cable.

Third, revenue and profitability remain on the rise with organic revenue growth from that business expected to be an industry-leading 6% this year, the same percentage expected for growth in funds from operations (FFO), too. Altogether, the company expects its role in the expansion of 5G networks to support dividend per share growth of 7% to 8% a year.

That would keep pace with the 8.5% in annualized dividend growth over the past three years. CCI stock currently yields about 3.4% at a share price of about $170, and analysts give it a price target of about $197. That seems reasonable going forward for this buy-and-hold equity.

Demand for warehouse space remains robust

Matt DiLallo (Prologis): Shares of Prologis have tumbled more than 30% from their recent peak. The catalyst was news that Amazon has more warehouse space than it currently needs. That's leading the e-commerce giant to shed at least 10 million square feet of space.

With Amazon flooding the market with excess warehouse space, it could cool off rental rates, which have been red-hot. Rents soared 20% globally last year. Prologis anticipated a similar growth in 2022 when it reported its first-quarter results shortly before the Amazon news.

While slowing rent growth would affect Prologis, the industrial REIT still has enormous embedded upside potential. For starters, most of its existing leases are currently 47% below market rates on average due to the long-term nature of its contracts. As those leases expire, Prologis can capture an additional $1.6 billion of net operating income (NOI) by signing leases at market rates, assuming no further growth in rent.

Meanwhile, the company is developing over $1 billion of new warehouse capacity to support the enormous long-term demand for warehouse space as e-commerce continues expanding. It has already leased a significant portion of its development pipeline, meaning they'll provide incremental rental income when they come online.

Finally, the company recently agreed to buy its largest rival, Duke Realty(NYSE: DRE), in a $26 billion deal. Duke also has a sizable gap between its current lease rates and market rents and a large development pipeline. Because of that, Prologis expects the deal will immediately boost its bottom line while enhancing its long-term growth prospects.

With shares of Prologis slumping, its dividend yield is approaching 2.7%, its highest level in years. That higher yield might not last long. Prologis' stock could bounce back quickly as investors realize the company has lots of upside, even if rent growth slows in the near term.

10 stocks we like better than Alexandria Real Estate Equities

When our award-winning analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and Alexandria Real Estate Equities wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of June 2, 2022

John Mackey, CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool's board of directors. Brent Nyitray, CFA has no position in any of the stocks mentioned. Marc Rapport has positions in Alexandria Real Estate Equities, Amazon, and Crown Castle International. Matthew DiLallo has positions in Amazon, Bristol Myers Squibb, Crown Castle International, Moderna Inc., and Prologis. The Motley Fool has positions in and recommends Amazon, Bristol Myers Squibb, Crown Castle International, and Prologis. The Motley Fool recommends Alexandria Real Estate Equities, Illumina, Moderna Inc., and Uber Technologies. The Motley Fool has a disclosure policy.