Gray Television (NYSE:GTN) Reports Q4 In Line With Expectations But

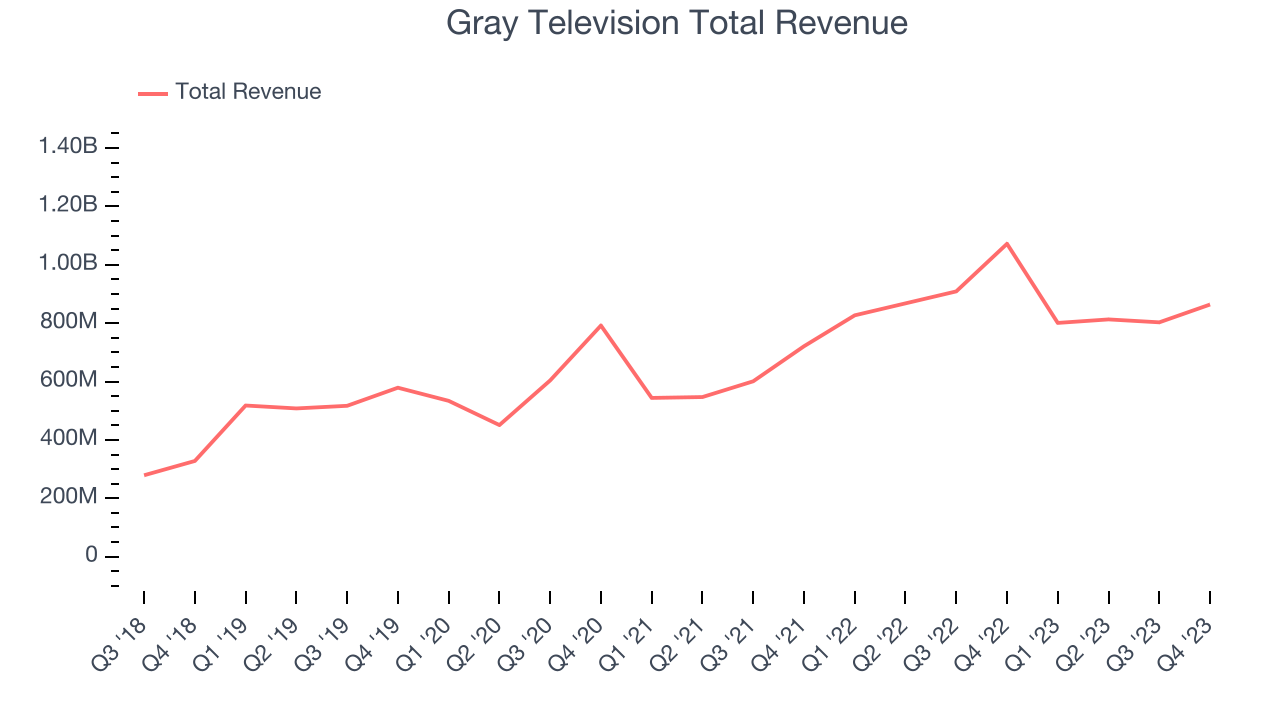

Local television broadcasting and media company Gray Television (NYSE:GTN) reported results in line with analysts' expectations in Q4 FY2023, with revenue down 19.4% year on year to $864 million. On the other hand, next quarter's revenue guidance of $820 million was less impressive, coming in 5.8% below analysts' estimates. It made a GAAP loss of $0.24 per share, down from its profit of $2.02 per share in the same quarter last year.

Is now the time to buy Gray Television? Find out by accessing our full research report, it's free.

Gray Television (GTN) Q4 FY2023 Highlights:

- Revenue: $864 million vs analyst estimates of $862.7 million (small beat)

- EPS: -$0.24 vs analyst estimates of -$0.15 (-$0.09 miss)

- Revenue Guidance for Q1 2024 is $820 million at the midpoint, below analyst estimates of $870.8 million

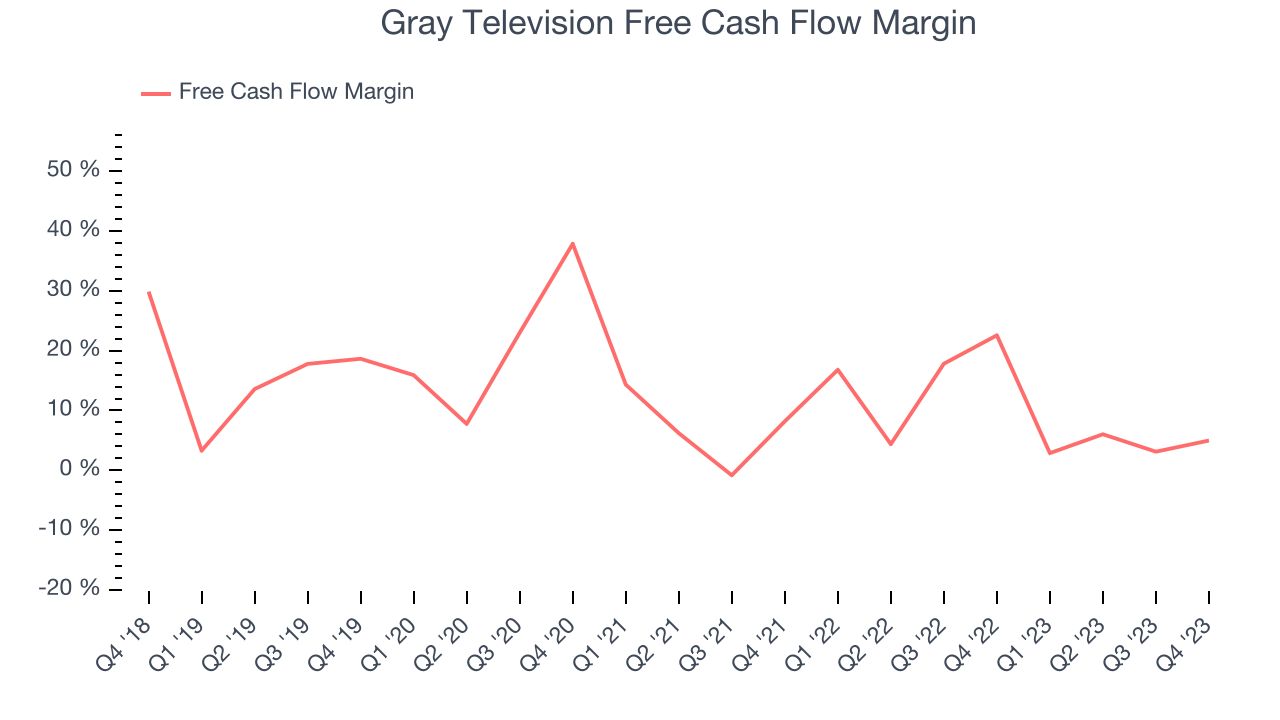

- Free Cash Flow of $43 million, up 72% from the previous quarter

- Gross Margin (GAAP): 27%, down from 44.4% in the same quarter last year

- Market Capitalization: $737.2 million

Specializing in local media coverage, Gray Television (NYSE:GTN) is a broadcast company supplying digital media to various markets in the United States.

Broadcasting

Broadcasting companies have been facing secular headwinds in the form of consumers abandoning traditional television and radio in favor of streaming services. As a result, many broadcasting companies have evolved by forming distribution agreements with major streaming platforms so they can get in on part of the action, but will these subscription revenues be as high quality and high margin as their legacy revenues? Only time will tell which of these broadcasters will survive the sea changes of technological advancement and fragmenting consumer attention.

Sales Growth

A company's long-term performance can indicate its business quality. Any business can enjoy short-lived success, but best-in-class ones sustain growth over many years. Gray Television's annualized revenue growth rate of 24.8% over the last five years was exceptional for a consumer discretionary business.  Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. Gray Television's recent history shows its momentum has slowed as its annualized revenue growth of 16.6% over the last two years is below its five-year trend.

Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. Gray Television's recent history shows its momentum has slowed as its annualized revenue growth of 16.6% over the last two years is below its five-year trend.

We can better understand the company's revenue dynamics by analyzing its most important segment, Retransmission. Over the last two years, Gray Television's Retransmission revenue (affiliate fees) averaged 23.1% year-on-year growth. This segment has outperformed its total sales during the same period, lifting the company's performance.

This quarter, Gray Television reported a rather uninspiring 19.4% year-on-year revenue decline to $864 million of revenue, in line with Wall Street's estimates. The company is guiding for revenue to rise 2.4% year on year to $820 million next quarter, improving from the 3.1% year-on-year decrease it recorded in the same quarter last year. Looking ahead, Wall Street expects sales to grow 19.7% over the next 12 months, an acceleration from this quarter.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Cash Is King

If you've followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills.

Over the last two years, Gray Television has shown decent cash profitability, giving it some reinvestment opportunities. The company's free cash flow margin has averaged 10.4%, slightly better than the broader consumer discretionary sector.

Gray Television's free cash flow came in at $43 million in Q4, equivalent to a 5% margin and down 82.2% year on year. Over the next year, analysts predict Gray Television's cash profitability will improve. Their consensus estimates imply its LTM free cash flow margin of 4.3% will increase to 15.2%.

Key Takeaways from Gray Television's Q4 Results

It was good to see Gray Television beat analysts' operating margin expectations this quarter. That stood out as a positive in these results. On the other hand, its revenue and EPS missed, and its revenue guidance for next quarter fell short of Wall Street's estimates.

The company noted it saw an improvement in the automobile advertising category, perhaps signaling the auto industry is emerging from its current downturn. Furthermore, it saw increased political advertising revenue as politicians gear up for the 2024 elections. Lastly, Gray Television's CFO, Jim Ryan, announced he would retire. He will stay with the company until 2025 and be replaced by Jeff Gignac, who will be in an Executive Vice President role until Ryan retires. Gignac was the former Head of Media & Telecom Investment Banking at Wells Fargo Securities.

Overall, this was a mixed quarter for Gray Television. The company is down 1.4% on the results and currently trades at $7.85 per share.

Gray Television may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.