3 AI Stocks Analysts Like Better Than C3.ai

Investors are constantly chasing the next big thing, and right now, nothing has them more hyped than artificial intelligence (AI). PwC researchers predict it'll be a game-changer, adding a whopping $15.7 trillion to the global economy by 2030. Playing a crucial role in this space is Redwood City, California-headquartered C3.ai, Inc. (AI), which develops AI algorithms that organizations integrate into their software infrastructure to speed up and automate tasks.

Valued at $2.7 billion by market cap, shares of C3.ai have seen quite the rollercoaster ride since they first hit the market on Dec. 9, 2020, at $42 each. Its stock soared to a record high of $183.90 per share that same month. Since that peak, the stock has taken a nosedive, plummeting more than 88%. Currently, it's sitting 56% lower than its 52-week high of $48.87. And the bad news keeps coming – it is down 25.6% on a YTD basis, lagging behind the S&P 500 Index's ($SPX)8.3% returns over the same time frame.

Given the investment risks associated with C3.ai, analysts are not very enthusiastic about the stock's prospects, giving it a consensus rating of “Hold.” For investors seeking exposure to the burgeoning AI industry, here are three low-priced AI stocks to consider now – all of which are favored by Wall Street analysts over C3.ai.

AI Stock #1: Guardforce AI Company

Guardforce AI Company (GFAI), based in Singapore, is a standout in the AI sector, specializing in security with a unique reliance on AI to ensure safety and efficiency. Its utilization of robotics-based security solutions truly sets it apart from its peers, and places it at the forefront of innovation. Although the company’s history dates back to 1982, it was only in 2020 that things got rolling in its AI-related business. That’s when Guardforce launched the T1 Robot as part of its Robotics-as-a-Service (RaaS) business and robotics AI solutions. Its market cap currently stands at $21.1 million.

Shares of GFAI are down 13.6% on a YTD basis. However, the stock still trades 40% above its 52-week lows.

The stock currently trades at 0.22 times sales – much lower than C3.ai, which is trading at 10.26x sales. Moreover, Guardforce trades at a discount to its other peers, like Senstar Technologies (SNT) and Wisekey International Holding (WKEY).

Most recently, the company reported an H1 2023 net loss of $13.8 million on Oct. 2, 2023, on revenue of $18.4 million. Its loss per share narrowed 39.2% year over year to $4.35. The company’s current assets increased to $42.1 million from $35.3 million, with a significant rise in cash and cash equivalents, which increased to $24.7 million from $6.9 million. Moreover, Guardforce completed the conversion of $15.91 million debt and interest into ordinary shares at $5.40 per share, which should improve the company's balance sheet.

Looking ahead, Guardforce is tentatively expected to report results for the full fiscal year this Friday, April 19.

GFAI has a “Strong Buy” rating, though there’s only one analyst in coverage at the moment. The price target for Guardforce is $14, assigned by EF Hutton in April, which indicates a potential upside of 389%.

AI Stock #2: Soundhound AI, Inc.

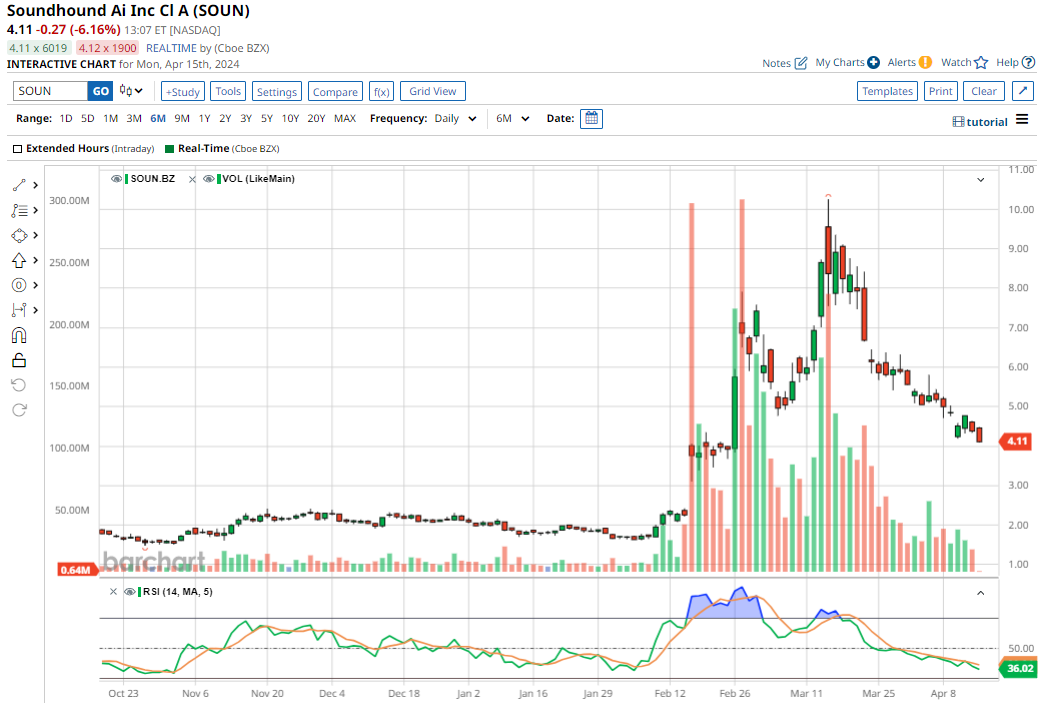

Headquartered in Santa Clara, Soundhound AI, Inc. (SOUN) develops independent voice AI solutions that enable the customer service industries' automotive, TV, and Internet of Things (IoT) businesses to deliver high-quality conversational experiences.

Valued at $1.4 billion by market cap, Soundhound stock has risen 95.3% on a YTD basis, massively outperforming the SPX’s gain over the same time frame.

Priced at 29.51 times sales, Soundhound appears to be expensive at current levels. Soundhound's stock price rally was fueled after chip giant Nvidia (NVDA) disclosed a $3.7 million investment in Soundhound in its 13F filing on Feb. 14. Nvidia's dominant role in AI made investors sit up and take notice when the tech giant showed interest in Soundhound.

However, Soundhound shares fell about 18% on March 1 as investors reacted to its Q4 2023 results. Its revenue increased by 80% year over year to $17.1 million, as cumulative subscriptions and bookings backlog (revenue to be recognized in the future) doubled to $661 million from the year-ago quarter. That said, Soundhound is yet to be profitable. It is striving to trim its GAAP net losses, which decreased from $0.15 to $0.07 in Q4.

Management pushed back its forecast for profitability by one year, projecting revenue to be around $70 million in fiscal 2024 and to achieve positive adjusted EBITDA by 2025, with revenue potentially exceeding $100 million. Analysts tracking Soundhound predict its revenue will grow by 51.5% year over year to $69.5 million in 2024, while GAAP losses are projected to narrow to $0.30 per share in fiscal 2024 and $0.21 in fiscal 2025 from $0.40 in 2023.

SOUN has a consensus “Moderate Buy” rating overall. Of the six analysts covering the stock, four recommend “Strong Buy,” and two suggest “Hold.” The average analyst price target for Soundhound is $7.15, indicating a potential upside of 73.5%. The Street-high target price of $9.50, assigned by DA Davidson in March, suggests 130.5% upside potential.

AI Stock #3: Sprinklr, Inc.

New York-based Sprinklr, Inc. (CXM), with a market cap of $3.2 billion, provides enterprise cloud software products worldwide. With advanced AI, Sprinklr's unified customer experience management (Unified-CXM) platform helps companies deliver human experiences to every customer. Sprinklr works with over 1,700 enterprises, including global brands like Microsoft (MSFT), P&G (PG), Samsung, and more than 60% of the Fortune 100.

Sprinklr stock is down 5.9% on a YTD basis.

CXM stock currently trades at 4.31 times sales – lower than C3.ai.

The stock fell more than 5% in one session when Sprinklr released its fiscal Q4 earnings report after the close on March 27. Sprinklr's revenue increased 17.5% year over year to $194.2 million, surpassing Wall Street projections by 2.9%. Plus, revenue via RPO, or remaining performance obligations, rose 24.8% sequentially to $966.6 million. Its non-GAAP net income per share of $0.12 also beat analysts' expectations by 133.3%. Around 126 customers spend over a million on the Sprinklr platform.

The company expects fiscal 2025 revenue to range between $804.5 million and $805.5 million, while non-GAAP net income per diluted share is projected to be between $0.38 and $0.39. Analysts tracking Sprinklr expect EPS to grow 47.1% in fiscal 2026.

CXM has a consensus “Moderate Buy” rating overall. Of the 14 analysts covering the stock, eight recommend “Strong Buy,” and six suggest “Hold.” The average analyst price target for Sprinklr is $16.64, indicating a potential upside of 46.6%. The Street-high target price of $22 suggests a 93.8% upside potential.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

Provided Content: Content provided by Barchart. The Globe and Mail was not involved, and material was not reviewed prior to publication.