Insurance executive Shenglin Xian, left, grocery tycoon Yuangsheng Ou Yang, and property developer Morris Chen, right, were ordered to sell their shares in Wealth One Bank. The bank, founded in 2016 and based in Toronto, caters to Chinese-Canadian clients.Supplied

Finance Minister Chrystia Freeland has instructed three of the founding investors of Wealth One Bank of Canada to divest their shares, and has also ordered the financial institution to comply with extraordinary national-security conditions intended to firewall its operations against the trio, who have faced federal scrutiny over alleged links to the Chinese government.

The three men, Toronto insurance executive Shenglin Xian, Vancouver property developer Morris Chen and Toronto grocery tycoon Yuangsheng Ou Yang, were told in April to sell their shares in the bank. Wealth One has also been ordered to sever all ties with the three, and to put in place stringent security measures to guard against money laundering and unauthorized sharing of sensitive information.

Wealth One, founded in 2016 and based in Toronto, caters to Chinese Canadian clients. The federal government approved it as a Schedule 1 bank, meaning it is considered a domestic institution, not a subsidiary of a foreign bank, and is authorized to accept deposits and provide mortgages. In a 2021 news release, it said it had grown into a financial institution with more than $400-million in assets. It was established with an initial investment of $50-million.

Ms. Freeland’s new restrictions on Wealth One are unlike any others placed on Canadian banks in recent history, and are being imposed at a time of heightened political tension over Chinese interference in Canadian domestic affairs. Her orders rely on powers outlined in the federal Bank Act that are designed to protect against threats to national security, international relations or the integrity of banks.

The government’s warnings to the three shareholders stretch back at least as far as November, when Ms. Freeland sent a letter telling them they could be susceptible to Chinese government pressure. She also raised concerns that the bank might have engaged in money laundering. Shortly after receiving the letter, the three men resigned as directors of the bank, but did not divest their shares in Wealth One.

The Globe and Mail reported in February that the bank and the three shareholders had been under investigation by the Canadian Security Intelligence Service since 2021 and, more recently, by officials in the federal Finance Department. The exact substance of these investigations, and the nature of any conclusions they may have reached, are not publicly known.

On April 24, Ms. Freeland issued amended letters of patent – or written orders – to Wealth One, which The Globe obtained through an access to information request with the Office of the Superintendent of Financial Institutions, Canada’s bank regulator. In those documents, Ms. Freeland ordered the bank to “sever as soon as reasonably practical, all banking relationships” with the three men, and with parties they control or are related to.

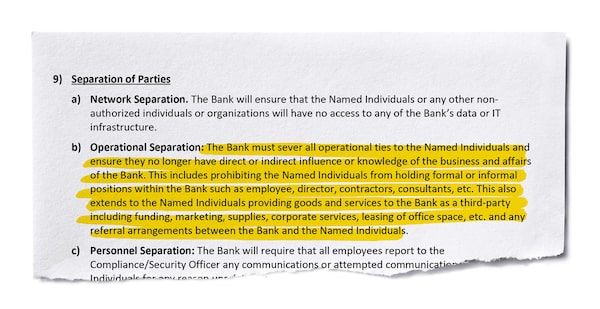

“This includes prohibiting the named individuals from holding formal or informal positions within the bank such as employee, director, contractors, consultants,” Ms. Freeland’s orders say. The three shareholders are also prohibited from providing goods or services to the bank “including funding, marketing, supplies, corporate services, leasing of office space, etc.”

In a separate letter also dated April 24, Ms. Freeland ordered the three men to divest their shares in Wealth One. It is unclear whether they have done so, or whether they will challenge the order in the court.

Paul Leonard, Wealth One’s president and chief executive officer, declined to say whether the divestment has happened. He said in a statement that the bank had worked collaboratively with Ottawa, and that it had proposed several of the terms that Ms. Freeland’s orders formalized.

“This brings certainty for the bank and closure for our stakeholders as we continue to operate in the normal course, under the leadership of our independent board of directors and the management team,” he said.

Attempts to reach Mr. Ou Yang and Mr. Chen were unsuccessful. Glen Jennings, a lawyer at Gowling WLG, which is representing Mr. Xian, said in a statement that his client “is in regular communications with the relevant authorities and expects a good outcome for all stakeholders that will benefit all Canadians.” He added that “matters relating to the Bank are regulated and under strict rules of confidentiality, and thus Mr. Xian has no comment to make at this time.”

Jessica Eritou, senior communications adviser to Ms. Freeland, declined to discuss the Finance Minister’s actions against Wealth One and its founders. She said Ms. Freeland “takes very seriously her responsibility for the security and stability of the Canadian financial sector.”

“As Minister of Finance, she is empowered to act to address risks to any bank in Canada, and risks posed to the Canadian financial sector,” Ms. Eritou said. “Given her role as a regulator, it would be inappropriate to comment on any specific process that may be under way.”

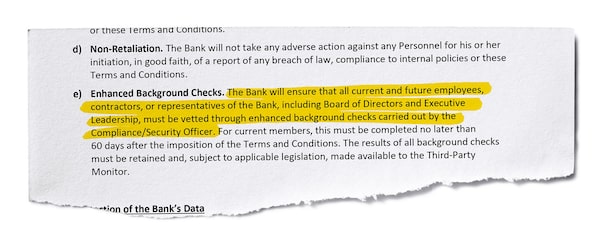

Other requirements Ms. Freeland has imposed on Wealth One include stringent national-security measures, such as vetting of all the bank’s employees, relocation of its Toronto headquarters to new secure premises and sweeps of its corporate property for surveillance devices. The institution is also prohibited from using the Chinese social-media messaging app WeChat for banking business.

Ms. Freeland has also instructed the bank to appoint an independent third-party monitor and hire two compliance officers: one for security compliance, with a valid national-security clearance, and one for anti-money-laundering and anti-terrorist compliance. Bank employees are being required to undergo what the Finance Minister’s directive calls “advanced training” in compliance with the Proceeds of Crime (Money Laundering) and Terrorist Financing Act, also known as the PCMLTFA, a federal law designed to stop terrorist financing and the illegal concealment of the origins of funding.

Former finance and national-security figures said they were unaware of any other instances of ministerial power being used to oust a Canadian bank’s founders and force it to adopt security measures. “I have never heard of anything like this before, certainly not in my lifetime,” former deputy minister of finance Scott Clark said. “When the minister goes to that length there is something very concerning about that bank.”

Former CSIS director Richard Fadden, who also served as national-security adviser to Prime Minister Justin Trudeau and his predecessor Stephen Harper, said it is clear that extraordinary measures were put in place to “match an extraordinary set of circumstances.”

According to land registry documents, Shenglin Xian currently owns Wealth One Bank’s 170 Sheppard Ave. E location in Toronto, pictured.Christopher Katsarov/The Globe and Mail

“I don’t see how it could be anything other than a national-security preoccupation on the part of the minister, and her measures are very detailed,” he said. “But measures like this do not guarantee the elimination of Beijing’s influence, because that can be manifest in any number of ways. That doesn’t mean that Mr. X, who holds position Y, doesn’t go off on the weekend and chat with people who may be providing guidance or influence.”

In March, the country’s anti-money-laundering watchdog, the Financial Transactions and Reports Analysis Centre of Canada (FinTRAC), announced that it had fined Wealth One $676,500 for failing to comply with the PCMLTFA. FinTRAC said the bank’s violations included failing “to submit suspicious transaction reports where there were reasonable grounds to suspect that transactions were related to a money laundering offence.”

Ms. Freeland’s conditions also prohibit the three founding shareholders, and parties related to or controlled by them, from accessing the bank’s data. If Wealth One becomes aware of an unauthorized attempt to access that information, it is required to report the breach within 15 days.

The bank’s staff are also required to report “any communications or attempted communications” by the three shareholders “for any reason unrelated to compliance with these terms and conditions.”

The founding shareholders are prohibited from entering Wealth One facilities under most circumstances. And Ms. Freeland is requiring the bank to ensure its offices and buildings are unconnected to the three men.

She is also requiring Wealth One to relocate from its Toronto headquarters “as soon as possible.” Land registry documents say the bank’s 170 Sheppard Ave. E location in Toronto is currently owned by Mr. Xian.

“Prior to signing a new purchase or lease agreement, this new location along with proposed physical security measures will be submitted to the minister for approval,” the conditions say.

In the interim, the bank is subject to strict surveillance measures. It is required to fit its offices with new alarms and cameras, and to disconnect any cameras owned by the building’s landlord. Ms. Freeland’s orders go into minute detail on the necessary arrangements.

Wealth One is required to sweep for surveillance devices “at all of the bank’s locations and for all corporate devices designated or approved for remote use.” The orders say this must be done immediately, and at least annually afterward, “to ensure the integrity of the bank’s independence and operations.”

And Ms. Freeland is requiring the bank to perform a quarterly “network-wide security scan” to identify any actual or potential security violations, or instances of data being shared with “an unauthorized third-party.”

The Globe first reported on Mr. Xian in May, 2016, when he and 32 other business executives attended a private fundraiser for the Liberal Party of Canada, where Mr. Trudeau was the guest of honour.

At the time, Mr. Xian was waiting for final approval from federal bank regulators to launch Wealth One as a Schedule 1 bank. That was granted a month later. Mr. Xian told The Globe in 2016 that he did not discuss Wealth One with Mr. Trudeau.

“Nothing, nothing, I just met him,” he said. “We never mentioned it. It was just … to say hi, that’s all. We never mentioned … Wealth One.”

Mr. Xian and Mr. Ou Yang have property and investments in China, according to information recently removed from the Wealth One website.

In 2016, Wealth One’s website contained incorrect information about Mr. Ou Yang’s biography. The bank claimed he had served as a member of China’s National People’s Congress, which is the country’s legislature, and the Chinese People’s Political Consultative Conference, a political advisory board to the Chinese government. This would have meant he was a powerful political figure in China before he came to Canada.

Wealth One told The Globe in November, 2016, that Mr. Ou Yang had belonged to neither of those bodies, and that his assistant had misrepresented her boss’s credentials and inflated his achievements.

In 2013, Mr. Ou Yang was sued by Barry Wan, a minority shareholder in his grocery business. Mr. Wan alleged in court documents that he was not paid his fair share from Yuan Ming, a supermarket in Mississauga, and that Mr. Ou Yang and his wife, Ming Zhu Zhuang, had committed “accounting irregularities.” A court later ordered Mr. Ou Yang to buy out Mr. Wan’s 10-per-cent interest in the business, according to Mr. Ou Yang’s lawyer, Andrea Habas.

Mr. Xian has faced legal disputes involving his insurance business. In 2013, the Insurance Council of British Columbia fined him $2,000 for proceeding with life-insurance policies for a married couple without getting proper written authorization for changes.

In 2003, two Chinese immigrants in Oakville, Ont., complained to Advocis, a national professional association for financial advisers, alleging Mr. Xian had duped them into putting $20,000 of their savings into the first-year premiums of three life-insurance policies they could not afford. Mr. Xian later left Advocis “after a dispute over the findings of disciplinary panels,” the Toronto Star reported in 2005.

Mr. Chen, along with his wife, Mingyan Lin, who is also a shareholder in Wealth One Bank, operate the North America Investment and Trade Promotion Association, which pushes for close economic ties between Canada, China and the United States.

In June, 2021, Wealth One announced that former Ontario Liberal finance minister Charles Sousa had joined its board. He departed in December, 2022. That same month, he was elected in a federal by-election as the Liberal member of Parliament for Mississauga – Lakeshore.

Robert Fife

Robert Fife Steven Chase

Steven Chase